Uncertainty, it seems, is our new normal.

U.S. President Donald Trump’s Covid-19 diagnosis has made an already messy election year even more chaotic, the U.K. and Europe are at risk of further lockdowns as coronavirus cases increase, and Brexit talks are still up in the air. In Asia, tensions are simmering between pro-democracy activists and the local government in Hong Kong while India’s underfunded health-care system is facing a growing challenge to control the virus outbreak.

Finding compelling reasons to invest when faced with so many unknowns is a daunting challenge — but one that our quarterly panel of veteran investors lives with every day. These money managers now see opportunities that stretch from cyclical stocks — which benefit when the economy runs hot — to battered European banks and the sovereign debt of China.

Before investing, build an emergency savings fund to see you through six months of expenses, if possible. If you’ve accomplished that already and can tick off the other suggestions in “The 7 Habits of Highly Effective Investors,” then you’re probably on solid financial ground.

For those who want to invest in the panelists’ themes using exchange-traded funds, Bloomberg Intelligence ETF analyst Eric Balchunas suggests ETFs that can serve as good proxies.

Sarah Ketterer

Chief executive officer and fund manager, Causeway Capital Management

Buy European Banks

Some of the global equity market’s worst performers for the year are bank stocks, especially in Europe. The largest, best-managed European lenders trade at record low valuations — yet their balance sheets are strong enough to absorb all but the most draconian of economic outcomes.

Investors have abandoned these stocks, in part because the banks have suspended dividends and share buybacks during the pandemic at the request of regulators — yet many of the companies are likely to again pay dividends next year. That resumption, along with a revival in buybacks, should reward shareholders for their patience.

European regulators are finally facilitating mergers between banks and encouraging them to become more profitable through consolidation. In September, two large Spanish banks announced they will combine to form the country’s largest lender.

What’s more, bank stocks can outperform even when interest rates are low. Between 2009 and 2015 — a period of particularly low rates in the U.S. — shares of U.S. lenders outperformed the S&P 500 index by more than 55%.

The average European bank trades at a miserly 40% of tangible book value. With a potential economic recovery, they should trade at 80% — that would mean a doubling in the share price, with room still for further increases.

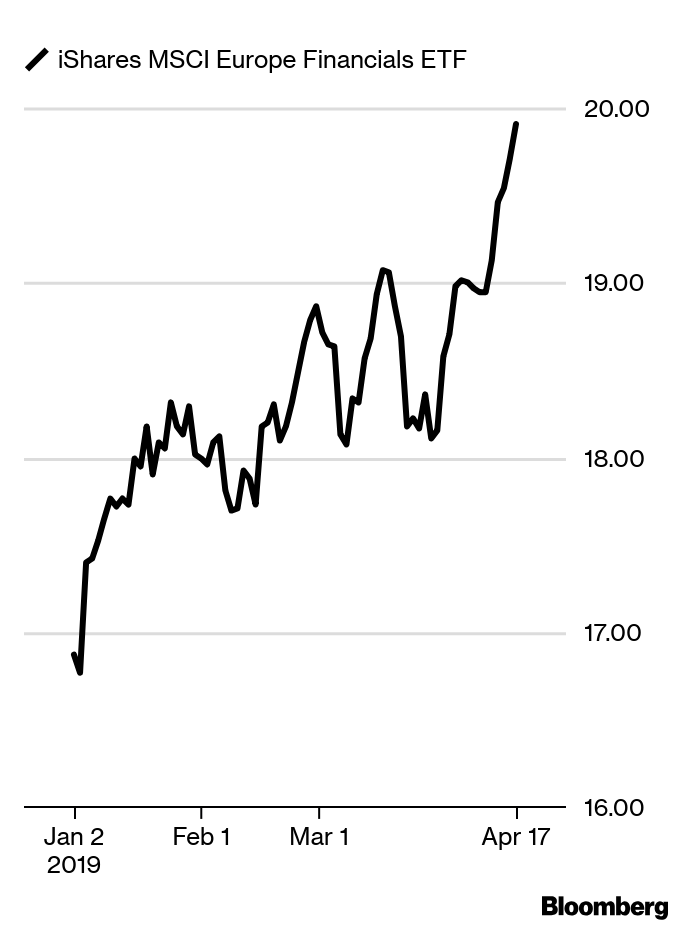

How to play it with ETFs: There are no ETFs focused only on banks, so Balchunas highlights the iShares MSCI Europe Financials ETF (EUFN). EUFN will benefit if European banks retrace some of their 2020 losses, as Allianz SE, HSBC Holdings Plc and BNP Paribas SA are among top holdings. The expense ratio is 0.48%.

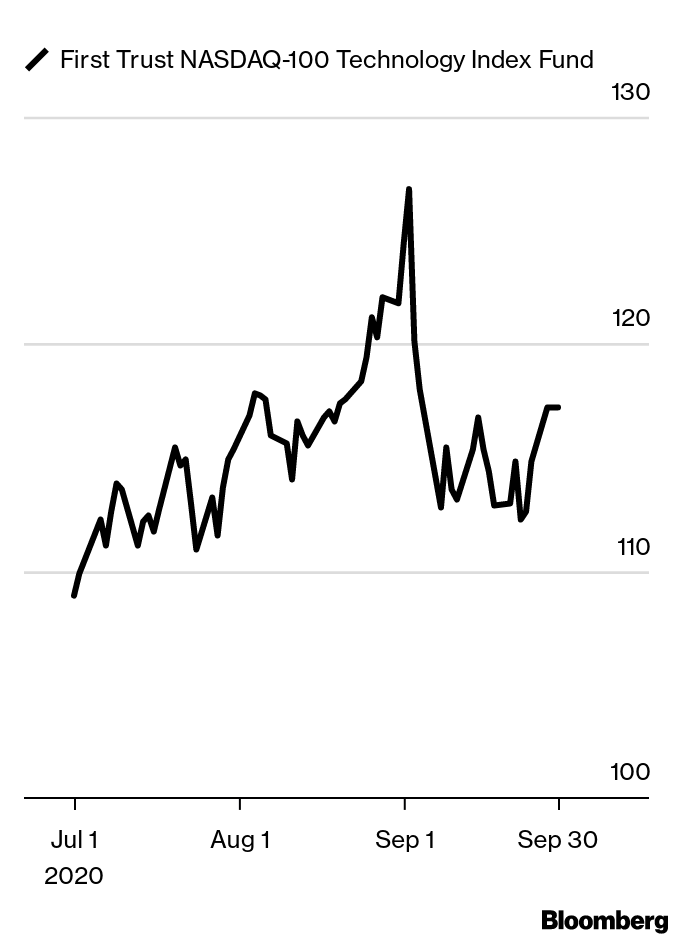

Performance of last quarter’s ETF plays: The First Trust Nasdaq-100-Technology Sector Index fund (QTEC) was up 7.4%.

was up 7.4%.

Look to Outsourcers

To temper volatility from cyclical stocks that are influenced by the economy, adding equities with consistent earnings growth seems prudent. A good example of this are companies that provide outsourcing for operations such as finance and accounting, reporting, web development, call centers, HR functions, marketing, and so on.

The industry has expanded at a pace slightly above global real GDP growth over the past several years, reaching total revenue of approximately $160 billion in 2019. Thousands of the world’s largest companies use those kinds of services in daily operations. In a Covid-19-induced recession, outsourcing becomes an imperative.

This type of business-process outsourcing began years ago with customer service call centers, often located in countries with low labor costs. It is evolving into digital transformation services, deploying artificial intelligence and automation, such as use of robot apps to automate processes and a virtual workforce. Companies that provide these services have sticky long-term annuity revenues, and the winners are expanding their profit margins as they add more sophisticated services.

How to play it with ETFs: The First Trust Nasdaq-100-Technology Sector Index Fund (QTEC) is loaded with B2B technology companies that are expanding more deeply into corporate services, and have the advantage of recurring revenue from software as a service models. The fund’s expense ratio is 0.60%.

is loaded with B2B technology companies that are expanding more deeply into corporate services, and have the advantage of recurring revenue from software as a service models. The fund’s expense ratio is 0.60%.

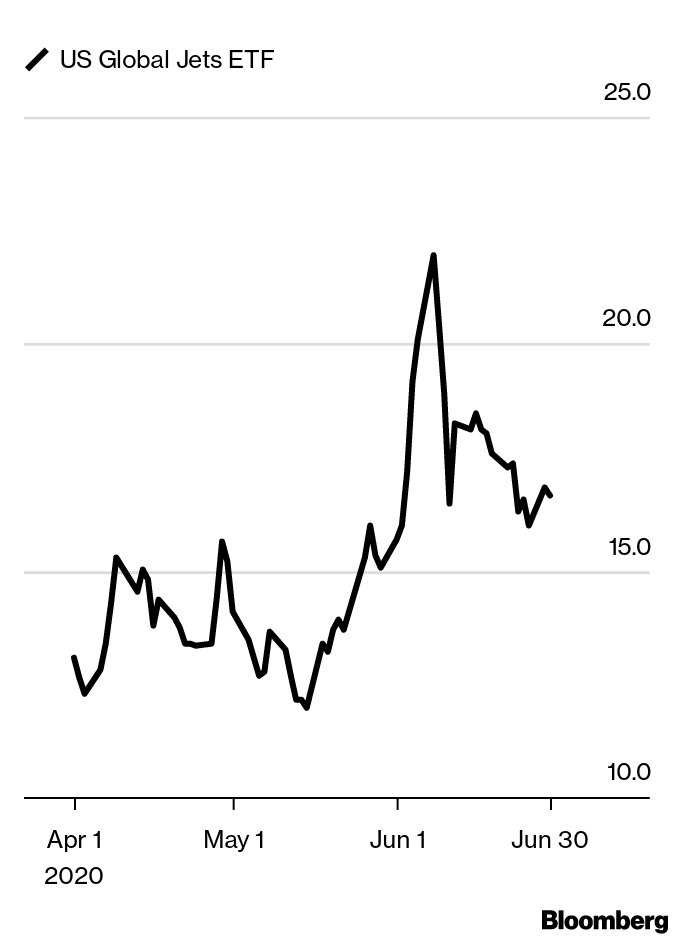

Performance of last quarter’s ETF plays: Balchunas’s pick for a way to invest in Ketterer’s theme last quarter was the US Global Jets ETF (JETS) , which rose 13.5% in the second quarter.

, which rose 13.5% in the second quarter.

Buy into Aero-mageddon

To help contain the coronavirus, most commercial flights are grounded. Countries that account for more than 98% of global passenger revenues have imposed travel restrictions. IATA, an airline industry association, recently forecast passenger traffic down 38% this year (this compares with the worst drop on record of -3.5% in 2009) and a 44% decline in passenger revenue. Every additional week of lockdown worsens this aero-mageddon. Despite the recent groundings, investors would do well to look ahead.

Global aviation and aerospace has strategic importance, facilitating billions of passenger journeys and transporting billions of dollars worth of cargo, not to mention military applications. Most governments are extending financial lifelines to their respective national aviation and aerospace industries. High fixed costs, emblematic of these industries, translates to a very wide moat.

World class aerospace companies boast expertly-engineered products/equipment/software, global manufacturing facilities and massive supply chains, while airlines hold scarce allocations of airport landing/departure slots. Strong players in aviation and aerospace have a network and franchise that’s incredibly difficult and expensive to replicate.

Airplanes will take to the skies again soon, as they enable free movement of people and goods globally. There are no alternatives. With testing and vaccines, plus some type of health certification, passenger demand will recover, amplified by the expanding middle class in emerging countries. Expect medical breakthroughs for society to jettison “social distancing” within a two-year investment horizon.

When unrestricted, airlines will re-accelerate fleet-modernization programs, purchase new fuel-efficient aircraft and become more sophisticated at data analytics. Those with weak balance sheets and uncompetitive offerings will disappear. Only two companies manufacture the majority of short- and long-haul aircraft, and four aircraft engine companies dominate the global market and service the bulk of the installed fleet.

Several well-managed airlines will likely take capacity from weaker rivals. The aviation ecosystem of catering, airport retail and the like have also seen their revenues collapse — yet many have very profitable franchises. Aviation and aerospace stocks, normally highly cash-flow-generating businesses, have performed miserably. U.S. and European aerospace stocks trade at historically low forward-valuation multiples. Many of these stocks must double to return to prices seen only last January, and several are poised to do even better.

How to play it with ETFs: The US Global Jets ETF (JETS) is a concentrated portfolio of U.S. passenger airlines. It has a 12% exposure to each of the four largest carriers and a 4% weighting for the next five largest. The rest of the portfolio contains global airlines, airports and aircraft manufacturers, all of which are facing the near-term demand shock from restricted travel. The fund’s positioning toward the largest and best-capitalized U.S. airlines is likely advantageous in the current contraction, Balchunas said, especially in light of potential fiscal aid.

is a concentrated portfolio of U.S. passenger airlines. It has a 12% exposure to each of the four largest carriers and a 4% weighting for the next five largest. The rest of the portfolio contains global airlines, airports and aircraft manufacturers, all of which are facing the near-term demand shock from restricted travel. The fund’s positioning toward the largest and best-capitalized U.S. airlines is likely advantageous in the current contraction, Balchunas said, especially in light of potential fiscal aid.

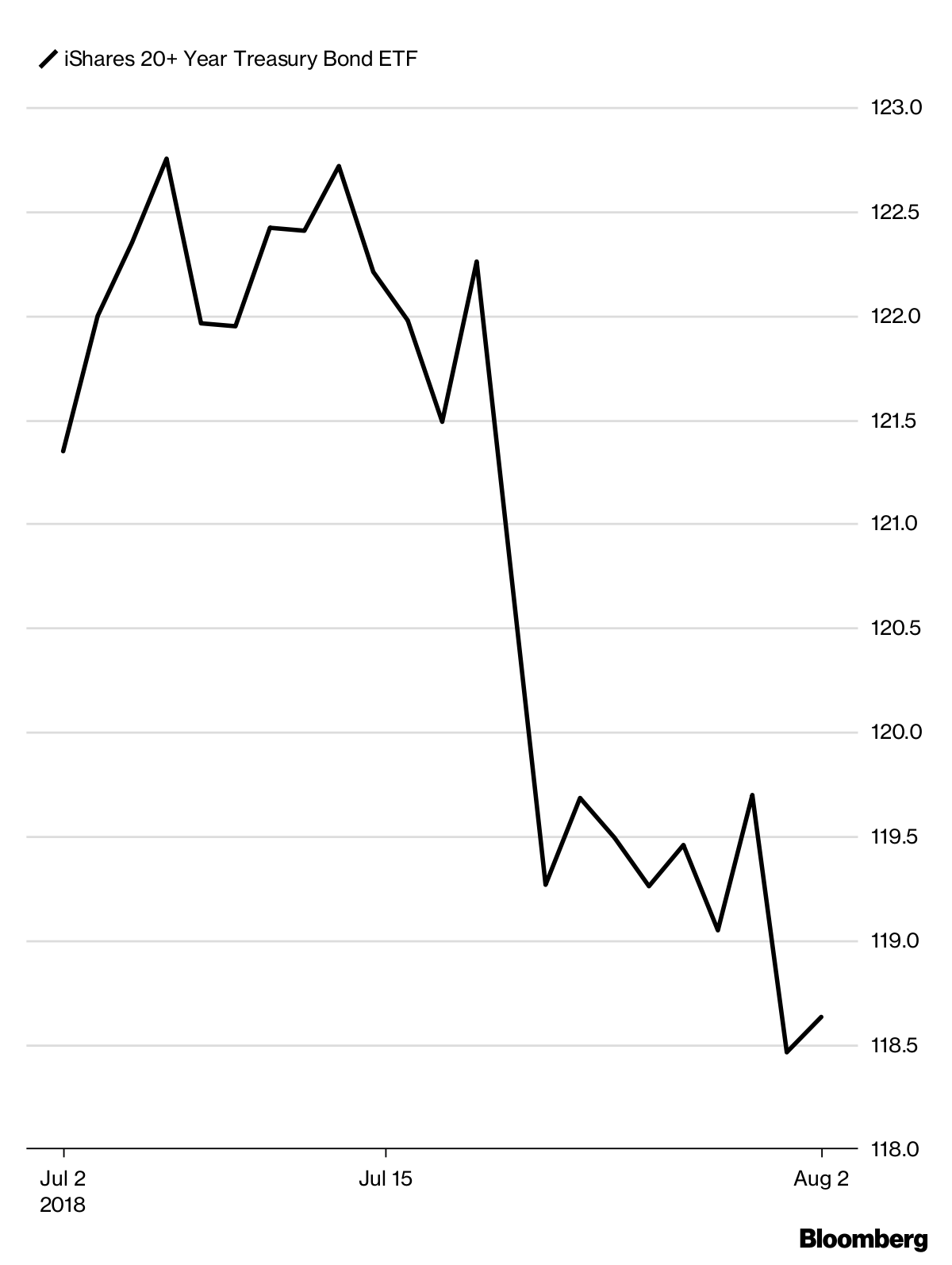

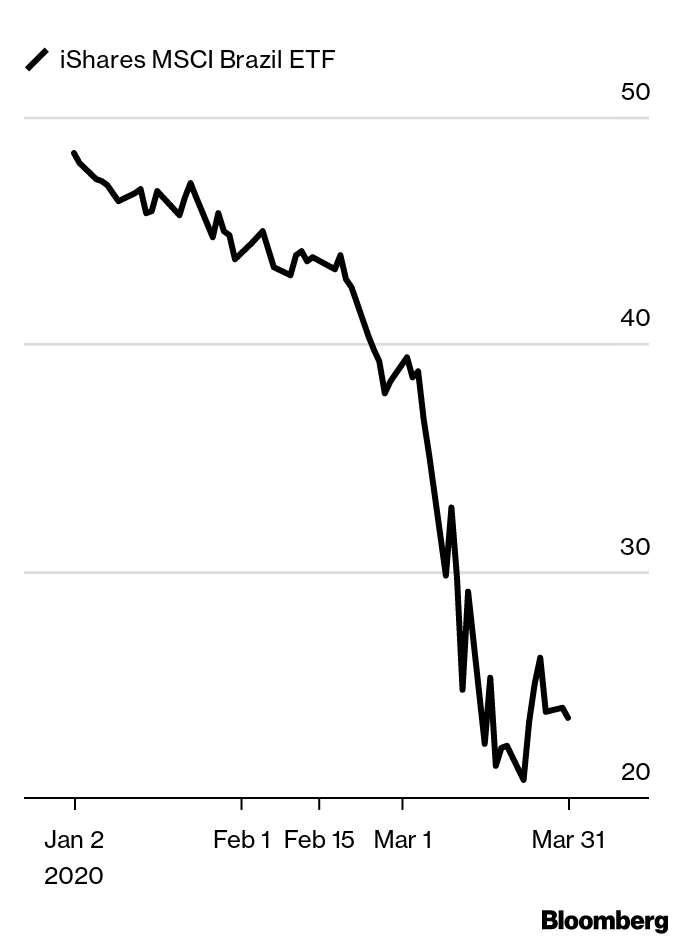

Performance of last quarter’s ETF plays: The iShares Global Energy ETF (IXC) felt the pain in the oil sector and fell 45.2%.

felt the pain in the oil sector and fell 45.2%.

Look to the Energy Sector

Despite an upturn in crude oil prices last year, 2019’s runaway bull market trampled global integrated oil majors. Energy makes up less than 6% of the MSCI All Country World Index and returned only 14% last year versus 27% for the Index. Even this month’s U.S. airstrike in Iraq and subsequent Iranian retaliation hasn’t attracted much buying interest in energy stocks. The MSCI World Integrated Oil & Gas Index trades below its 10-year low in price-to-cash flow multiples, with several constituents offering dividend yields well above 5%. But the oil majors, especially the Europeans, will likely experience enough upstream production in 2020 to accelerate their revenue growth.

Meanwhile, Iran sanctions may shrink global supply by 1.8 million barrels per day. OPEC production cuts may also support crude oil prices near current levels. U.S. shale drillers—the big swing factor in non-OPEC production—are struggling to access capital, thereby limiting their production. With a slowing of liquified natural gas (LNG) capacity and demand for LNG by the global shipping industry to curb emissions, natural gas prices could rise, boosting revenues for oil majors.

Managements have become disciplined in spending on expansion and in assiduous cost control. European oil majors have reduced their capital expenditures to about 37% below their peak in the 2011-2014 period. Global oil majors continue to slash costs and generate free cash flow (that’s cash not needed in operations). To satisfy investors, the oil and gas industry must pay attractive dividends, buy back shares and continue investing in low-carbon businesses such as solar, wind, biofuels and electric vehicle charging. Several of these European majors have published long-term carbon emissions reduction goals, with some committing to reductions of 50% or more by 2050.

In a world where central banks have created mountains of monetary liquidity and investors expect double-digit percentage annual returns from stocks, these steady oil majors can’t compete. For many investors, the prospect of a few percentage points of capital gains plus 5% or more in dividend yields must look rather dull. But dull might be just the right answer in the next few years.

How to play it with ETFs: Balchunas says that while there is no European energy ETF (yet), the iShares Global Energy ETF (IXC) tracks oil majors from all over the world. It holds stocks such as Exxon Mobil, Chevron and BP, and has a little more than 20% of the fund in Europe. It has $863 million in assets and a fee of 0.46%.

tracks oil majors from all over the world. It holds stocks such as Exxon Mobil, Chevron and BP, and has a little more than 20% of the fund in Europe. It has $863 million in assets and a fee of 0.46%.

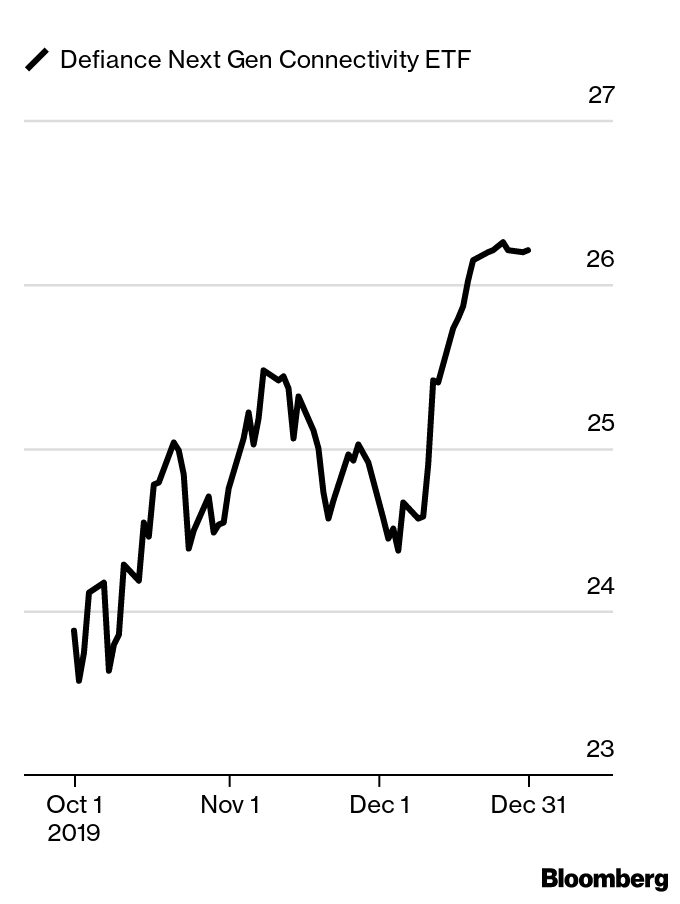

Performance of last quarter’s ETF plays: The Defiance Next Gen Connectivity ETF (FIVG) was Balchunas’s choice as a way to play Ketterer’s “factory of the future” theme. It had a 7.1% gain for the quarter.

was Balchunas’s choice as a way to play Ketterer’s “factory of the future” theme. It had a 7.1% gain for the quarter.

The Factory of the Future

With recession fears weighing on cyclical stocks globally, this may provide an excellent opportunity to buy some of Europe’s best industrial automation companies at relatively low valuations versus U.S. peers.

Advanced economies are on the doorstep of a 5G (5th generation cellular wireless) era of connectivity. Relative to the prior generation, 5G brings greater speed to move more data, lowers latency to boost responsiveness and connects a lot more devices.

In the next few years, this should help manufacturers move towards “Industry 4.0,” where connectivity and sensors augment machines connected to a system making both production and design decisions. This allows manufacturers to respond quickly to changing market dynamics with minimal disruption to production and make the entire value chain more efficient.

For example, if a product defect becomes apparent in the market, data regarding that flaw can be fed back into the factory to adjust the design and manufacturing process. Industry 4.0 will incorporate the smart factory: the latest fully automated flexible robotics capable of assembling products, 5G wireless technologies and industrial IoT (internet of things).

IoT is the network of physical objects and devices (such as computers, machines and robots) connected to the internet to collect and share data. Industrial automation will connect products and systems on the factory floor, as well as industrial assets in the field, through the cloud, allowing them to communicate to optimize design and production. This should lead to more productive factories and higher quality operations, not to mention better products.

A state-of-the-art automotive plant, for example, uses industrial automation technologies to design the optimal robotics path to boost weld quality and productivity. Sensors collect real-time data and can feed information about the production process from the later stages of manufacturing back into the earlier stages of design and manufacturing. In this factory of the future, people and collaborative robots work side by side. Global leaders in industrial automation will transform manufacturing and—as they succeed—attract considerable investor attention.

How to play it with ETFs: Defiance Next Gen Connectivity ETF (FIVG) offers exposure to companies developing the 5G networking and communication technologies. The fund has 18% exposure to non-U.S. companies. Top constituents are Skyworks Solutions, Analog Devices, Marvel Technology Group and Nokia Oyj. The expense ratio is 0.30%.

offers exposure to companies developing the 5G networking and communication technologies. The fund has 18% exposure to non-U.S. companies. Top constituents are Skyworks Solutions, Analog Devices, Marvel Technology Group and Nokia Oyj. The expense ratio is 0.30%.

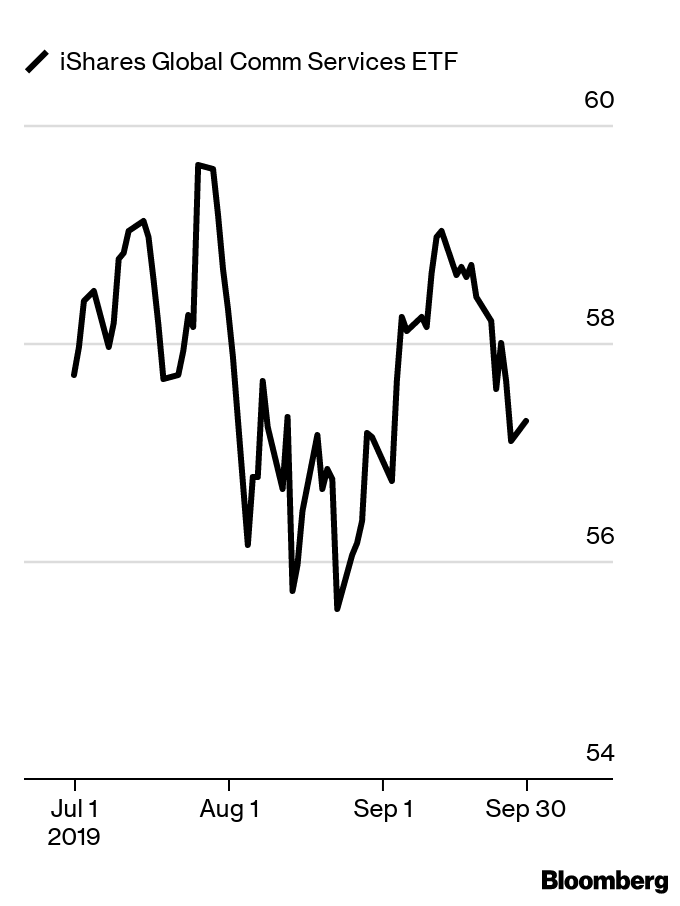

Performance of last quarter’s ETF plays: iShares Global Communications Services ETF (IXP) ended the quarter down 0.4%.

ended the quarter down 0.4%.

Look to Global Telcos

Equity markets don’t typically deliver double-digit percentage annual returns each year for 10 consecutive years. As of June 30, the U.S. and many foreign markets have achieved that feat. Super-normal returns reflect the tsunami of global monetary liquidity bidding up asset prices.

In this long-running bull market, investors seek growth and appear indifferent to valuation. For example, the percent of IPOs of companies with negative earnings in the past year exceeds the late 1990s technology bubble highs.

Rather than chase market winners—especially those in traditionally defensive sectors such as utilities and consumer staples—investors can find cheaper havens elsewhere. The unpopular global telecommunication stocks may have the right characteristics. Revenue growth for the telco industry should accelerate in the next few years as customers consume more data at an increased pace. A wider usage of additional devices—such as smart watches and a second mobile phone for work—is also driving up data usage and subscriber growth.

In Asia, the larger countries tend to have three telco competitors controlling the bulk of market share and enjoying favorable regulation. Several of these stocks trade at extremely low valuations relative to their markets and their own history. In Europe, the telco companies have acquired spectrum in various countries, defended their market positions against telco upstarts and are consolidating operations to improve returns.

For Europe to commercialize world-class 5G mobile telecommunications, the regulatory environment must become more supportive of the telco service providers. In all geographies, telco competitors will likely collaborate on infrastructure investments, sharing the cost of mobile phone towers. Meanwhile, many of the better-managed of these companies generate abundant surplus cash flow, and reward investors with generous dividends, which equate to yields well in excess of market averages.

Way to play it with ETFs: Balchunas’s choice is the iShares Global Communications Services ETF (IXP) , which he expects will benefit from growth in telcos both domestic and international. It has direct exposure to three of Europe’s largest carriers, Deutsche Telekom, Telefonica, and Vodafone Group, as well as China Mobile and Japan’s NTT

, which he expects will benefit from growth in telcos both domestic and international. It has direct exposure to three of Europe’s largest carriers, Deutsche Telekom, Telefonica, and Vodafone Group, as well as China Mobile and Japan’s NTT

Docomo. The fund is market-cap weighted, with 34% international exposure and an expense ratio of 0.47%.

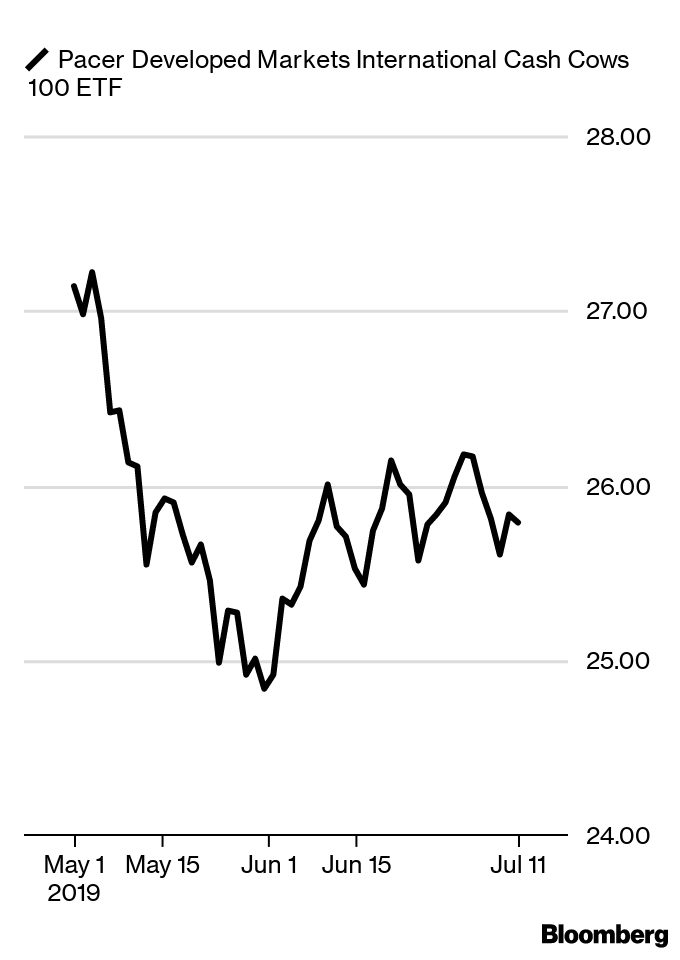

Performance of last quarter’s ETF plays: The Pacer Developed Markets International Cash Cows 100 ETF (ICOW) fell 1.3% in the second quarter.

fell 1.3% in the second quarter.

Look for the Tide to Turn

Cycles tend to turn when least expected. The past decade of massive global monetary accommodation has produced side effects such as asset inflation, fiscal deficits and rising levels of private and public sector debt. The excess liquidity effect in public equity markets has encouraged investors to care less about valuation—and more about growth.

Yet, as the pace of liquidity expansions slows, valuation will matter. Over the past decade to March 31, the U.S. market has returned almost 16 percent annually on average, a generous result for a developed-markets index. And it’s generous, indeed, given the shrinking risk, measured by near-record-low volatility.

Value stocks have underperformed growth for much of this post-2008 period, resulting in historically wide gaps between value indexes and growth indexes. From the year 2000, cheap stocks in the MSCI All Country World Index have outperformed expensive stocks by more than 40 percent over the next 12 months when the earnings yield spread (earnings yield of cheap stocks minus earnings yield of expensive stocks) has been in the top decile. At the end of March the earnings yield spread was in the 92nd percentile. At some point, extreme levels of depressed valuations will inspire buyers to snap up bargains.

The most undervalued stocks in many markets globally discount recession and structural disruption. Banks, maligned in a period of falling interest rates, trade at near-crisis levels, especially European ones. Global auto stocks trade at meager valuations versus history and compared with other cyclical segments of the markets, such as capital goods. Energy stocks are also trading at historically depressed levels.

For many growth stocks, earnings and cash flow are promised far into the future, which makes them the most sensitive to interest-rate fluctuations. As rates rise, these types of stocks typically swoon. In contrast, companies that generate surplus cash flow today, and return much of that to shareholders, offer immediate returns. With liquidity ebbing, a bird in the hand will (once again) be worth two in the bush.

Way to play it with ETFs: Balchunas points to Pacer Developed Markets International Cash Cows 100 ETF (ICOW) . The ETF offers international equity exposure to 100 securities with high free-cash-flow yields. ICOW has an expense ratio of 0.65 percent.

. The ETF offers international equity exposure to 100 securities with high free-cash-flow yields. ICOW has an expense ratio of 0.65 percent.

Performance of last quarter’s ETF plays: The iShares MSCI Europe Financials ETF (EUFN) , Balchunas’s pick to play on Ketterer’s theme of buying battered European bank stocks, rose 7.1 percent.

, Balchunas’s pick to play on Ketterer’s theme of buying battered European bank stocks, rose 7.1 percent.

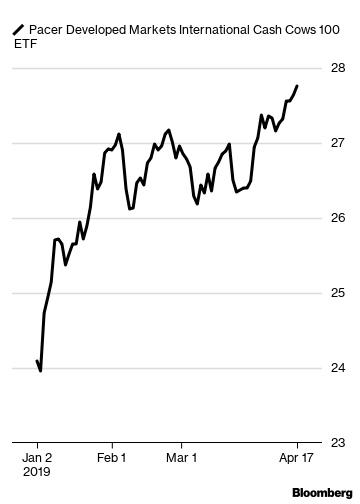

There’s a Price for Everything

By the close of 2018, global equity markets had punished—more like pulverized—stocks with economically cyclical earnings and typically rewarded those in the most defensive industries. The defensive havens included stocks in such industries as utilities, household and personal products, food and staples and retailing. In contrast, banks and insurance stocks, especially those in Europe, fell in price so sharply that their valuations have reached levels consistent with a severe recession and a financial system crisis.

That’s a value investor’s dream: to buy stocks whose valuations already discount an unlikely scenario, and then wait for the inevitable recovery. Even better, the most battered of European bank stocks pay investors to be patient via generous dividends.

Early this month, the MSCI Europe Banks Net Total Return USD Index traded at a multiple of eight times 2019 earnings and 0.7 times book value, and had a dividend yield of almost 6 percent. But these are not the same banks as during Europe’s last banking crisis. These companies have strengthened their capital positions to have four times as much capital as a decade ago. U.K. banks have enough capital, according to their regulator, to withstand an economic collapse, a huge rise in U.K. unemployment, a 33 percent drop in residential property prices and a 27 percent devaluation of the pound sterling. That’s akin to multiple shocks, and even after that nightmare, the banks would have twice the required capital.

Admittedly, banks are leveraged into economic conditions, good or bad. Adept bank managers (and there are plenty of these in Europe) know how to use their two primary levers to improve shareholder returns: cost control and capital management. With disciplined lending, ultra-cost efficiency and savvy technology spending, these well-capitalized banks should have a rosy future. At these bargain valuations, misery is already priced in.

Way to play it with ETFs: The closest thing to a play on European banks is the iShares MSCI Europe Financials ETF (EUFN) , which is made up of 60 percent banks. The ETF has a fairly reasonable expense ratio of 0.48 percent. Since the ETF is market cap-weighted, big players such as HSBC Holdings and Banco Santander make up a big chunk of holdings.

, which is made up of 60 percent banks. The ETF has a fairly reasonable expense ratio of 0.48 percent. Since the ETF is market cap-weighted, big players such as HSBC Holdings and Banco Santander make up a big chunk of holdings.

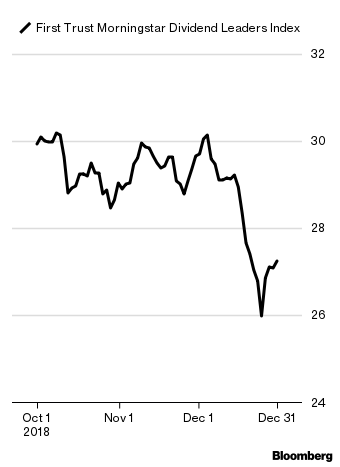

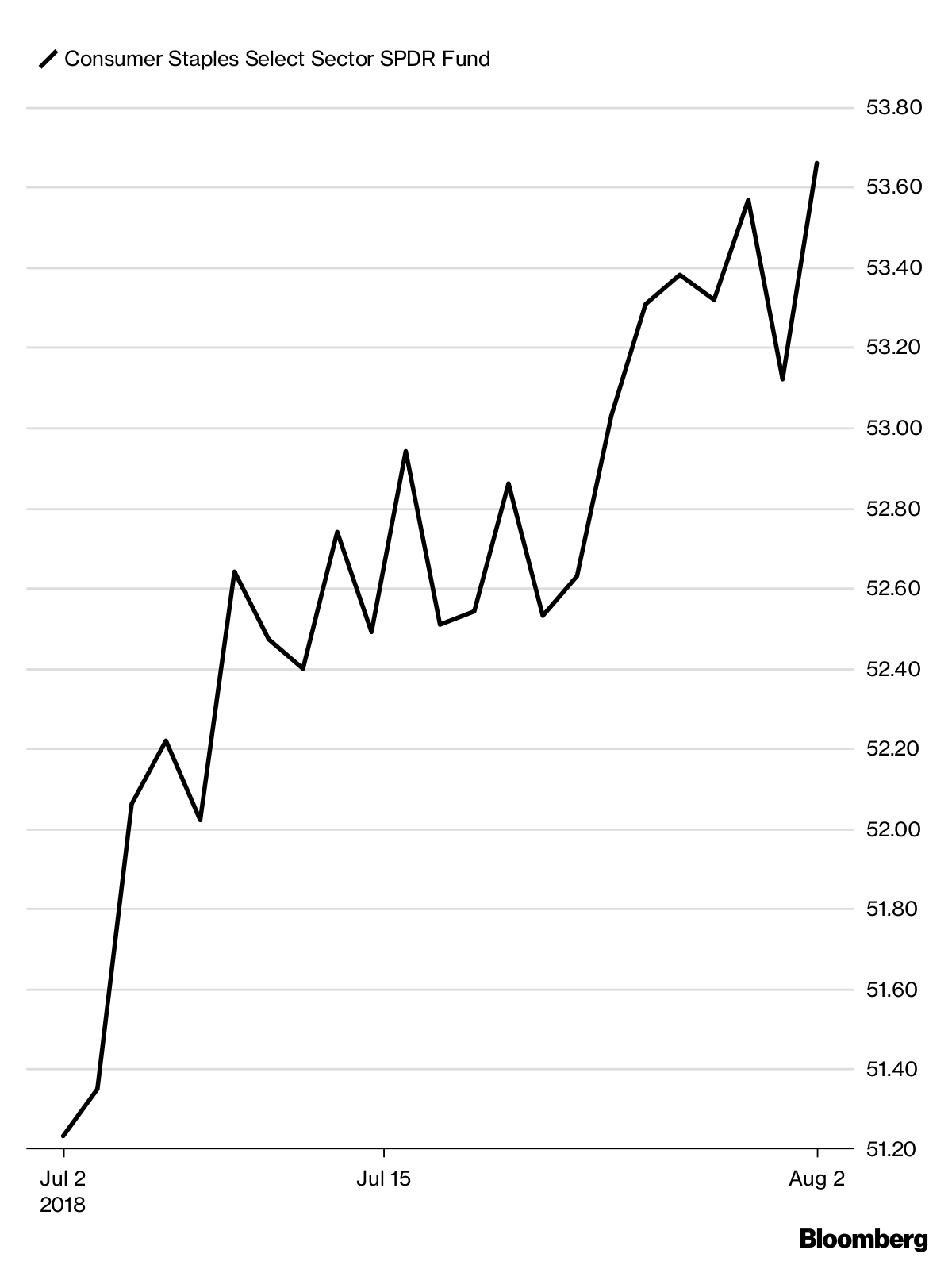

Performance of last quarter’s ETF plays: The First Trust Morningstar Dividend Leaders Index Fund (FDL) fell 9 percent in 2018’s final quarter.

fell 9 percent in 2018’s final quarter.

Cash Today Beats Cash Tomorrow

High-dividend-yielding, undervalued stocks may finally reign over growth stocks. In this global environment of gradually tighter monetary policy, the cash that a company returns to its shareholders in the next few years may be much more valuable than a potentially unfulfilled promise of rapid growth in profits many years ahead.

The massive growth in liquidity created by global central banks after the financial crisis has stalled in 2018, and will likely shrink in 2019. Meanwhile, valuation spreads between expensive and cheap stocks, measured by relative price-to-earnings ratios, are at extremely wide levels vs. history. In the past 20 years, these especially wide valuation spreads typically led to a narrowing of the gap and subsequent outperformance of cheap stocks.

The global consumer staples sector contains some of the cheapest, highest-dividend-yielding stocks. Many of these companies generate mountains of near-term cash flow. Within staples, the most maligned and possibly misunderstood segment is tobacco. Both U.S. and European-listed large-cap tobacco stocks trade at sizable discounts to their history. The discount may stem from investor concerns about the FDA’s tobacco regulation, shrinking U.S. cigarette volumes, a surge in demand for alternative products such as e-cigarettes and weakness in emerging market economies and currencies.

Much of this may be transitory, leaving investors with well-managed consumer marketing giants able to transition to a growing e-cigarette category. Heavily-taxed (and clearly very unhealthy) combustible cigarettes will likely disappear in the years ahead, replaced by less harmful forms of nicotine delivery. The more that global regulators focus their efforts on vapor, the better for these large incumbent tobacco companies, which are better able to absorb the costs of regulation than new entrants. Even in the shift to noncombustible products, global tobacco giants have the financial strength and prolific free cash flow generation to reward shareholders today and invest for tomorrow.

Way to play it with ETFs: Balchunas suggests the First Trust Morningstar Dividend Leaders Index Fund (FDL) which screens for stocks that have shown dividend consistency and then picks the 100 highest-yielding names. It’s heavy in consumer staples stocks, with big tobacco companies among top holdings. The $1.4 billion ETF charges 0.45 percent.

which screens for stocks that have shown dividend consistency and then picks the 100 highest-yielding names. It’s heavy in consumer staples stocks, with big tobacco companies among top holdings. The $1.4 billion ETF charges 0.45 percent.

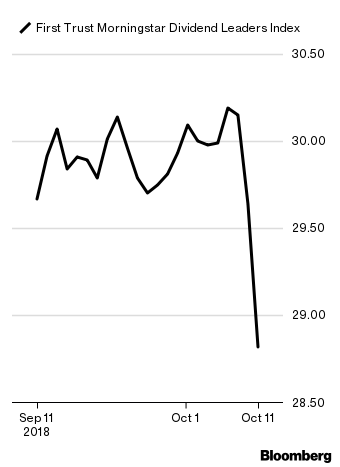

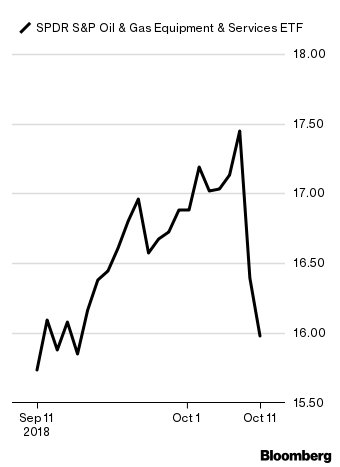

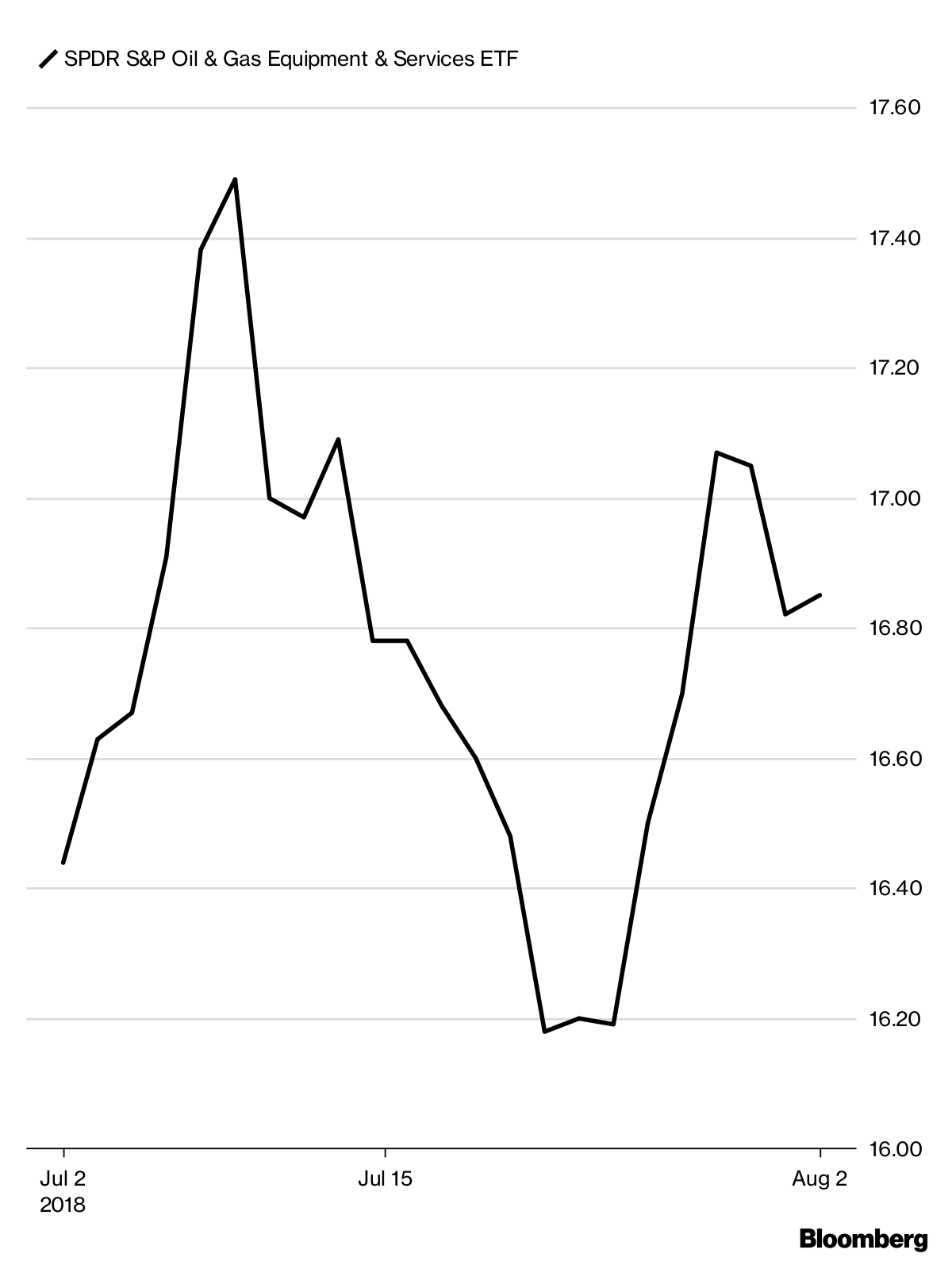

Performance of last quarter’s ETF plays: Balchunas pointed to the SPDR Oil & Gas Equipment & Services ETF (XES) as a way to play Ketterer’s suggestion of oilfield services companies. The ETF rose about 1.5 percent in the third quarter.

as a way to play Ketterer’s suggestion of oilfield services companies. The ETF rose about 1.5 percent in the third quarter.

Check Out Oilfield Services Companies

Despite the recovery over the past year in crude oil prices, some energy-related equities can’t seem to shake investor skepticism.

One of the most undervalued areas of the U.S. unconventional oil and gas industry is oilfield services. Of the onshore oilfield service stocks, the pressure pumpers have sagged significantly in price.

Pressure pumping is closely tied to drilling rig activity and is used in development of oil fields. After the well is drilled, pumpers mix water, sand and chemicals, then blast it into the reservoir rock so that the hydrocarbons will flow. Aided by technological improvements, producers have exceeded even their own expectations.

In the Permian Basin of western Texas, producers have extracted oil faster than the pipeline infrastructure can transport it to Gulf refineries and port terminals. The Permian Basin, notable for its enormous supply of crude oil and gas, has no near-term answer to these serious transportation bottlenecks. However, the problem should disappear in 2019 with the addition of pipeline capacity.

Investors, apparently unwilling to wait, have cast aside oil services stocks, especially those with sizable exposure to the Permian Basin. But pipeline squeezes don’t last long in the shale era; they incentivize midstream companies to accelerate new pipelines or expand existing capacity to fill the gap.

Meanwhile, oil prices seem well supported. New crude oil discoveries since 2013 probably can’t offset the drag from aging oilfield production declines, falling reserves and insufficient replacement of produced volumes. Supply constraints in countries such as Venezuela, Iran, Libya, Nigeria and Mexico may get worse.

As a recent affirmation of U.S. shale’s promising future, energy majors are making sizable acquisitions of U.S. onshore oil and gas assets. Producers will need oil services companies—even the beleaguered pumpers—to develop these newly acquired fields.

Way to play it with ETFs: To play the oil services industry, investors could use the SPDR Oil & Gas Equipment & Services ETF (XES) , an equal-weighted basket of large, mid- and small-cap oil services companies; its expense ratio is 0.35 percent.

, an equal-weighted basket of large, mid- and small-cap oil services companies; its expense ratio is 0.35 percent.

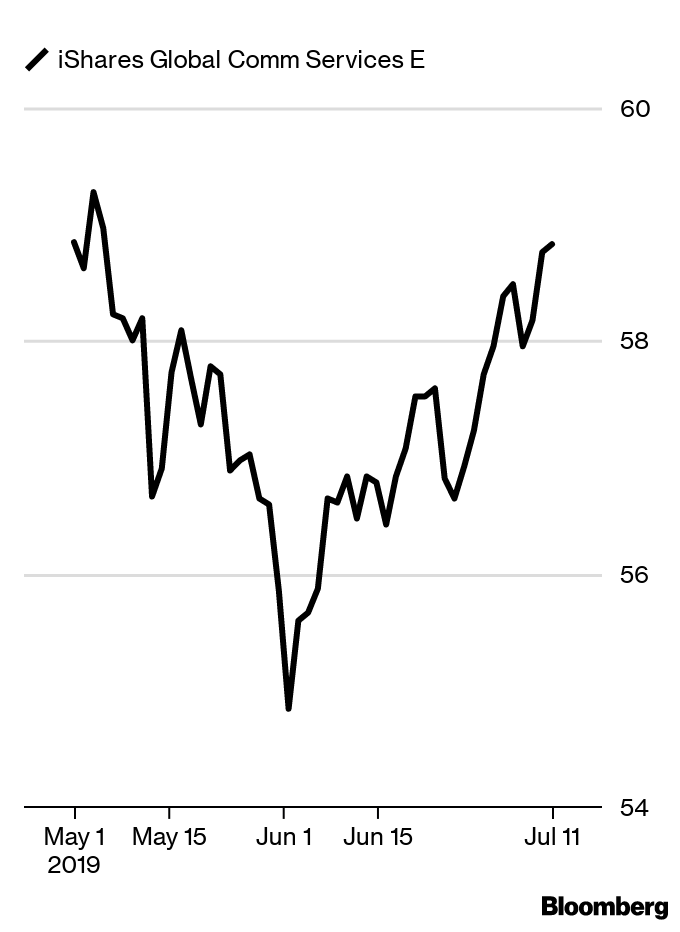

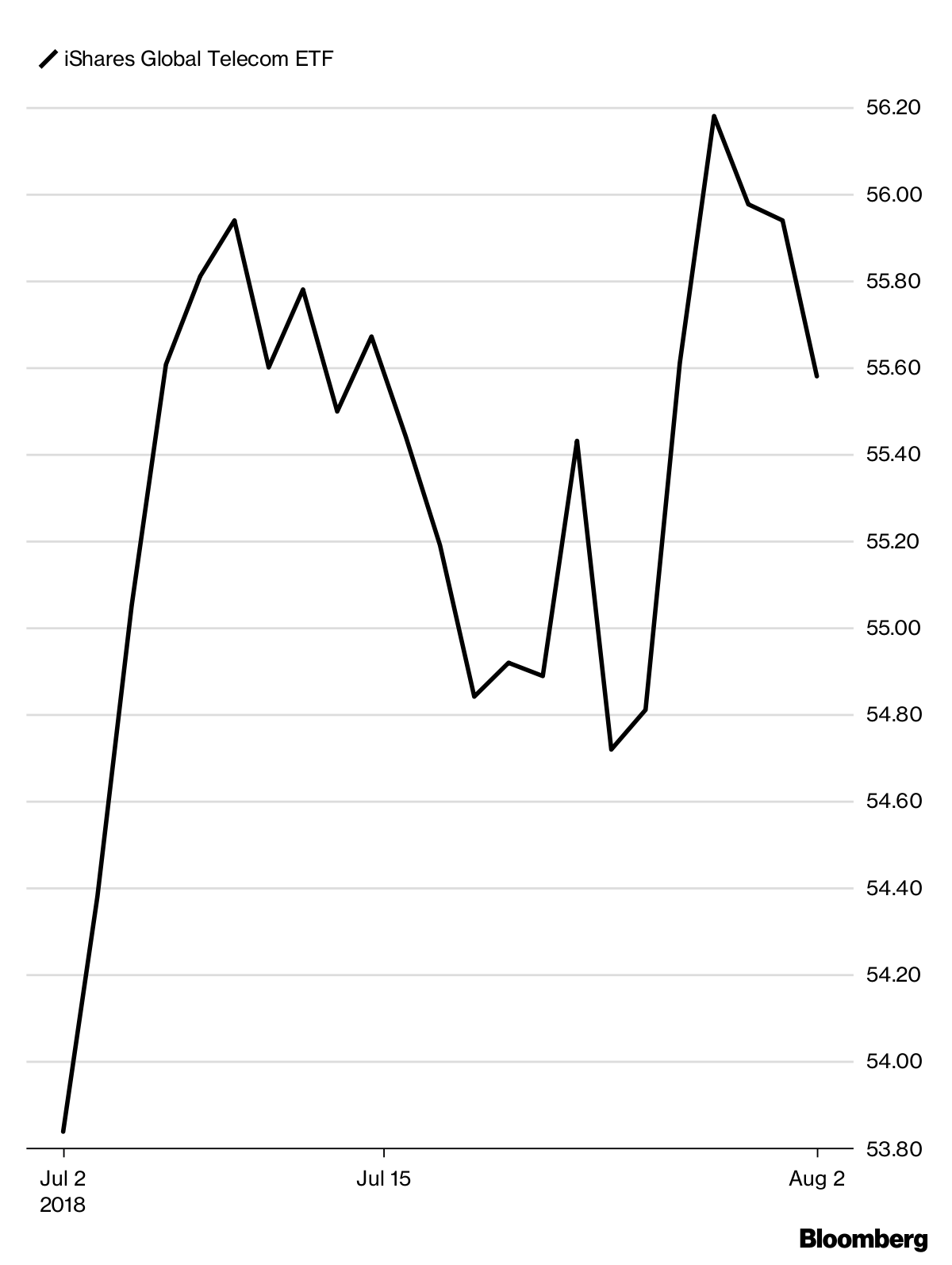

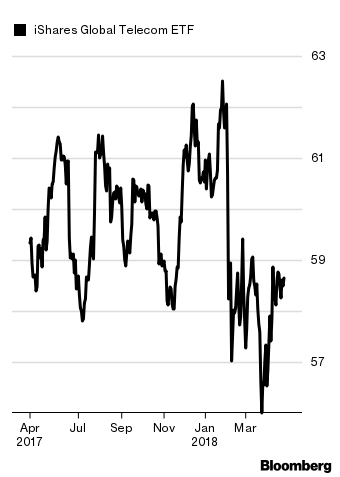

Performance of last quarter’s ETF plays: The iShares Global Telecom ETF (IXP) , which Balchunas chose as one way to play on Ketterer’s investing themes in the second quarter, dropped 5.7 percent in value over the quarter.

, which Balchunas chose as one way to play on Ketterer’s investing themes in the second quarter, dropped 5.7 percent in value over the quarter.

Go for Defensive Value

There’s a lot to be said for investment income, especially delivered via companies that are fully capable of sustaining that income for many years ahead. In sagging stock markets, some portion of an investor’s portfolio needs to produce returns now, not later. With plenty of dividend income, the wait for a market recovery shouldn’t seem quite so painful. Peer inside the global telecommunications sector and you will find many generous dividend payers also boasting financial strength far in excess of overall market averages.

These telecom stocks, unloved for their lack of recent growth and bland forecasts, have lost the interest of bull market investors. Mention Tencent or Alibaba and people will listen intently; refer to China Mobile or SK Telecom for yawns of boredom. Yet telecom behemoths offering mobile and fixed broadband services should grab our attention as ideal ballast for the inevitable bear markets. We need the services they offer—and will need them even more when fifth-generation wireless systems (5G) become commercially available.

The MSCI All Country World Telecommunications Services Index is made up of 81 constituents in developed and emerging-markets countries. By one valuation measure, enterprise value-to-Ebitda, it trades at a discount of more than 40 percent, compared with the aggregate equity market benchmark, the MSCI All Country World Index. (Enterprise value includes debt and cash when calculating company value, rather than just multiplying a company’s shares outstanding by its share price to arrive at market capitalization; Ebitda, a cash flow measure, refers to earnings before interest, taxes, depreciation and amortization.) The index also has a dividend yield almost 50 percent higher than the benchmark.

If sustainability of dividend yield makes you sleep better at night, focus on the companies with very low (or zero) net debt, defined as a company’s long-term debt less cash. In capital-intensive industries such as telecommunications, larger company size brings scale economies and cost advantages. Competitive, mature telecom markets typically cannot support more than three players, or returns on capital will decline for all participants. China, Japan and South Korea are three of the most attractive mature telecom markets globally.

Three-player telecom markets, in which competitors typically don’t engage in devastating price wars, often have stable participants generating reliable streams of cash. Companies rewarding shareholders by returning capital, through dividends and share repurchases, are less likely than growth-oriented peers to squander shareholder capital through overpriced acquisitions. Many telecom companies have learned that stability is one of their most attractive characteristics.

Way to play it with ETFs: There is no ETF tracking the MSCI All Country World Telecommunication Services Index, but Bloomberg Intelligence analyst Eric Balchunas says there is something very close: The iShares Global Telecom ETF (IXP) tracks 43 telecom stocks from about a dozen countries. It is notable for its high dividend yield of 3.5 percent, says Balchunas—and for its above-average fee (for a sector ETF) of 0.47 percent.

tracks 43 telecom stocks from about a dozen countries. It is notable for its high dividend yield of 3.5 percent, says Balchunas—and for its above-average fee (for a sector ETF) of 0.47 percent.

Performance of last quarter’s ETF plays: Balchunas chose the Vanguard Utilities ETF (VPU) and the Global X Lithium & Battery Tech ETF (LIT)

and the Global X Lithium & Battery Tech ETF (LIT) as ways to play Ketterer’s suggestion that investors consider global utility stocks. In 2018’s first quarter, VPU fell 4.1 percent and LIT tumbled 15.3 percent. LIT fell as analysts turned bearish on lithium, fearing a supply glut, as well as possibly less demand for electric vehicles in 2019.

as ways to play Ketterer’s suggestion that investors consider global utility stocks. In 2018’s first quarter, VPU fell 4.1 percent and LIT tumbled 15.3 percent. LIT fell as analysts turned bearish on lithium, fearing a supply glut, as well as possibly less demand for electric vehicles in 2019.

Think Smart Power

Utility stocks around the world have generally trailed their respective equity market performance over the past year. In the U.S., rising interest rates will push up utility borrowing costs, and corporate tax reform won’t boost earnings if the tax benefit must be passed on to customers. But just look a few years ahead, and the prospects for electric utilities may be considerably brighter than they are today.

The global conversion of internal combustion engine vehicles to electric vehicles (EVs, including plug-in hybrids) will boost the demand for electricity delivered efficiently to public charge points and homes. If large concentrations of EVs were to charge in the same hour, demand could spike to several times the norm, overloading the grid, causing overheating and blackouts. To avoid this, many electric utilities, especially in countries determined to reduce carbon emissions, will need to increase power utility investments substantially.

With new capacity, utilities may find it more efficient and cost-effective to provide power to large industrial customers, possibly operators of autonomous vehicle fleets, where recharging can be centralized rather than scattered across countless garages and parking spots. Electric utility regulators should allow the utilities to earn a healthy return on grid upgrades, new connections (such as new power lines to electrify parking bays), smart architecture, digitization and new peaking capacity. According to Goldman Sachs, these will be big global investments: $2.6 trillion for charging infrastructure to support full passenger vehicle electrification, plus another $3 trillion spent by the utilities for transformers, new lines and smart infrastructure.

Without a proper reconfiguration of a country’s electricity distribution grid, as well as security of electricity supply, the EV rollout simply cannot happen. This effort to build infrastructure for a massive global conversion to EVs should benefit electric utilities able to distribute low-cost power incorporating renewables such as solar and wind.

Way to play it with ETFs: For a cheap and deep utilities ETF, the Vanguard Utilities ETF (VPU) tracks 77 utility stocks for a fee of 0.10 percent. A more out-of-the-box but related play on the move to electric vehicles is the Global X Lithium & Battery Tech ETF (LIT)

tracks 77 utility stocks for a fee of 0.10 percent. A more out-of-the-box but related play on the move to electric vehicles is the Global X Lithium & Battery Tech ETF (LIT) . It tracks lithium miners and battery producers and has a fee of 0.76 percent.

. It tracks lithium miners and battery producers and has a fee of 0.76 percent.

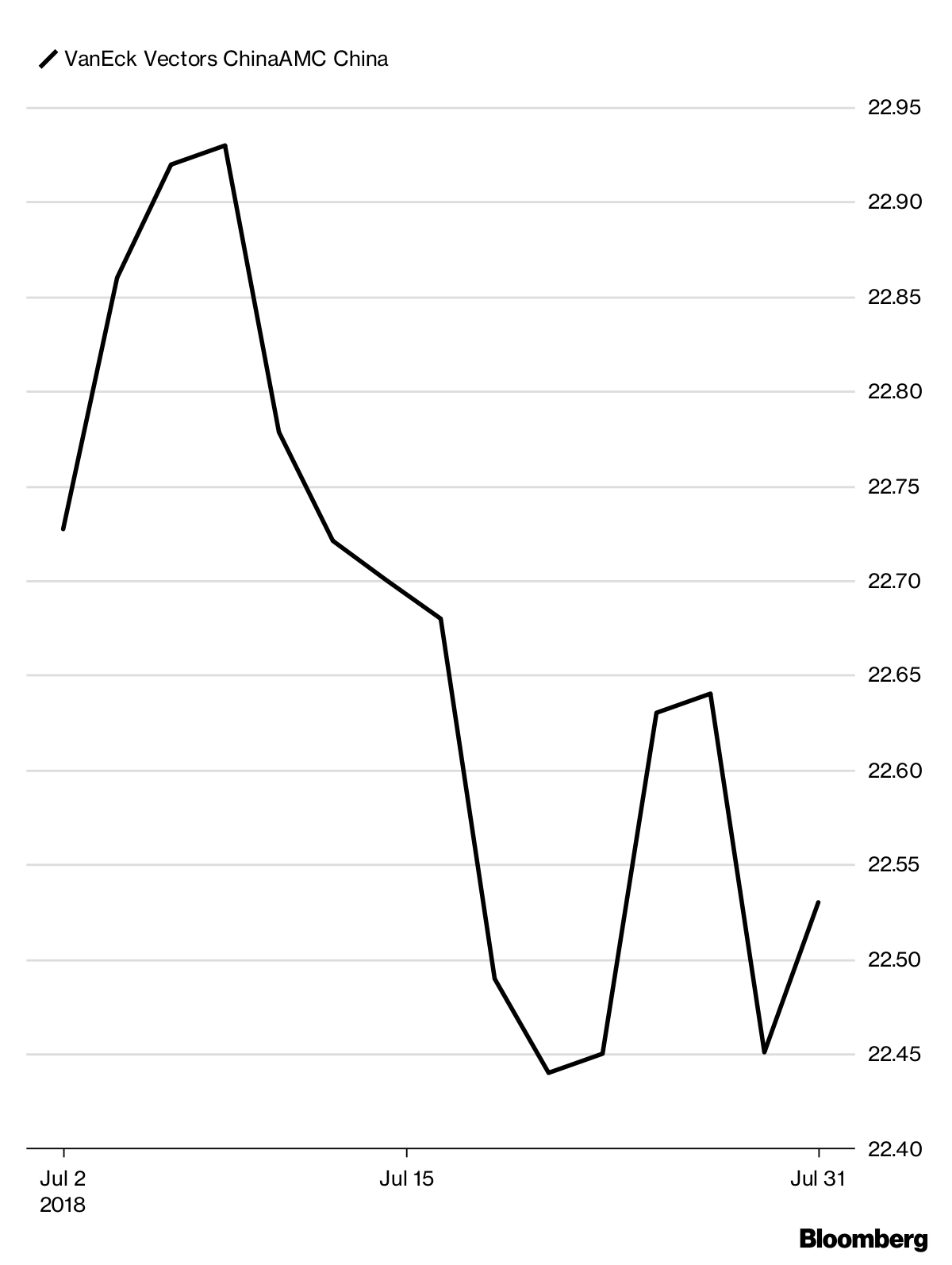

Performance of last quarter’s ETF plays: Last quarter, the ETF that was the closest fit for Ketterer’s theme of investing in China’s health care demand was the Global X China Consumer ETF (CHIQ) , which had about 8 percent of assets in the sector. In 2017’s final quarter, it gained 8.7 percent.

, which had about 8 percent of assets in the sector. In 2017’s final quarter, it gained 8.7 percent.

Invest in China’s Health Care Demand

Shifting from an emerging to a developed country, China can’t escape its demographics. As a byproduct of the one-child policy, China’s enormous population increased at only 0.6 percent per year from 1996 to 2015. That compares with the U.S. population’s expansion of 0.9 percent a year over the same period.

Low growth implies an aging population, and aging has its societal costs. Many Americans are struggling to pay for health care, and the Chinese are facing an even bigger tab. By 2050, roughly a quarter of China’s citizens will be older than age 60. With less than 6 percent of gross domestic product spent on health care (vs. 9 percent to 12 percent in most developed countries), the Chinese will likely devote more of their resources to staying healthy.

With rising disposable income per capita, China’s demand for health care, especially top-tier hospital services, exceeds supply. The central government recognizes the problems and aims to relieve congestion at the most reputable public hospitals by welcoming private capital into the industry. This flow of funds should improve conditions and spawn many higher-quality private hospitals. Other reforms include the elimination of unneeded middlemen in drug distribution, as well as prohibiting the markup of drug and medical devices.

Hospitals had become heavily dependent on drug sales to keep the lights on. To supplement their measly salaries, doctors accepted prescription-related bribes from pharmaceutical manufacturers. After a successful pilot program, zero markup of drugs became reality for most hospitals across the country this year. To speed up the approval process for efficacious drugs, the China Food and Drug Administration quadrupled its staff in 2015-16 and is on track to increase staff by 50 percent this year.

China’s health-care industry reforms, combined with the inevitable consolidation or demise of smaller or weaker players, will likely result in much greater efficiency and profitability in such areas as hospital management, drug and medical equipment distribution, private supplemental health insurance, and new-drug discovery and launch.

To complement reforms, the Middle Kingdom boasts a rising supply of young scientific talent, who are paid about a third as much as their peers in the developed world. Add to the mix a 15 percent corporate tax rate plus government subsidies to spur innovation, and the investment landscape looks very promising for Chinese health-care companies. (The standard Chinese corporate income tax rate is 25 percent, but the rate could be reduced to 15 percent for qualified enterprises engaged in industries encouraged by the Chinese government. Indigenous Chinese health-care companies are included in that category.)

Way to play it with ETFs: There are many China ETFs but none specific to the health-care sector, and most broad China ETFs have next to nothing in health-care exposure. The ETF with the most exposure to health care is the Global X China Consumer ETF (CHIQ) , which has about 8.7 percent of its assets in the sector.

, which has about 8.7 percent of its assets in the sector.

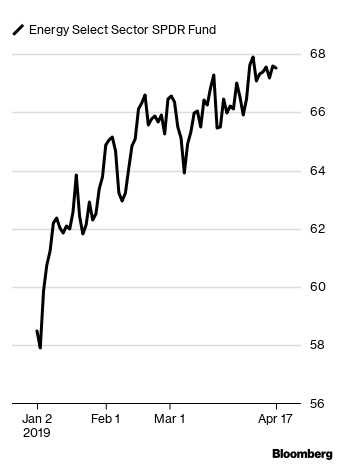

Performance of last quarter’s ETF plays: The Energy Select Sector SPDR Fund (XLE) rose 5.6 percent in the quarter ended Sept. 30. Top holdings Chevron Corp., Schlumberger Ltd., and Exxon Mobil Corp. rose 12.6 percent, 6 percent, and 1.6 percent, respectively.

rose 5.6 percent in the quarter ended Sept. 30. Top holdings Chevron Corp., Schlumberger Ltd., and Exxon Mobil Corp. rose 12.6 percent, 6 percent, and 1.6 percent, respectively.

Fuel Up on Energy

Buy high-quality energy. Investor skepticism weighs heavily on the sector, making this one of the more promising areas in this mature bull market.

Oil and gas companies exhibit cyclicality in sales and earnings, traits that investors have shunned in recent years in favor of steady growth. Relative to high-flying technology stocks, the recent performance of energy equities looks abysmal. Over the past 12 months, global energy indexes have underperformed global technology by more than 30 percent and are trading at a sizable valuation discount.

The forces of supply and demand dictate the price of semiconductors as well as oil, with the lowest marginal cost producers having a distinct advantage over the competition. Advertising, including the internet, also has a cycle. The last time markets ignored the cyclicality of technology was in the late 1990s, a rough period for the most overvalued stocks.

Investors may be worried about a global glut of crude oil, especially from rising U.S. shale oil production. U.S. shale productivity continues to surprise on the upside, especially in the Permian Basin. As marginal costs have fallen from 2014, oil producers have increased wells and drilling volumes. The threat of a possible lack of OPEC production discipline also clouds the oil price outlook.

But exploration and production costs have recently turned upward in pressure pumping, sand, rail, trucking and labor. Oil-producing nations, including OPEC members as well as U.S. shale producers, cannot afford to spend more cash than they generate. As industry profits get squeezed, oil and gas companies’ credit ratings deteriorate, constricting lending to energy. At current spot prices, the world’s oil and gas industry doesn’t generate enough cash flow to sustain the spending required to expand capacity. In U.S. shale, production volumes per well decline particularly rapidly without additional investment.

On the demand side, the energy industry will not thrive in a recession. But technology doesn’t fare well in that scenario, either. Expect at least two more decades of rising demand for crude oil and gas, as electric vehicles will only gradually substitute for gasoline.

Look for companies with productive acreage and experienced management, financial strength, and cyclically low valuations. As the crude oil price recovers—perhaps approaching $60 per barrel, with natural gas reaching $3.25 per thousand cubic feet—energy sector share prices should prove rewarding.

Way to play it with ETFs:The Energy Select Sector SPDR Fund (XLE) is high-quality energy. Top holdings Exxon Mobil Corp., Chevron Corp., and Schlumberger Ltd. make up more than 40 percent of the portfolio. There’s a liquid market for the ETF, and it’s cheap, with a fee of 0.14 percent.

is high-quality energy. Top holdings Exxon Mobil Corp., Chevron Corp., and Schlumberger Ltd. make up more than 40 percent of the portfolio. There’s a liquid market for the ETF, and it’s cheap, with a fee of 0.14 percent.

Performance of last quarter’s ETF plays: The SPDR S&P International Health Care Sector ETF (IRY) was Balchunas’s pick as a way to play Ketterer’s focus on big pharma companies selling at a discount. It returned 7.9 percent from Mar. 31 to June 30.

was Balchunas’s pick as a way to play Ketterer’s focus on big pharma companies selling at a discount. It returned 7.9 percent from Mar. 31 to June 30.

Buy the Pharma Discount

Why do several of the large global pharmaceutical stocks trade at above-market dividend yields and below-market price/earnings ratios? Perhaps the repeated threats by President Trump to cut drug prices have scared investors.

The president will likely claim victory for something that is already happening. The large buyers of U.S. pharmaceuticals, such as pharmacy benefit managers and health insurers, continue to exert tremendous pressure on drug companies to discount prices. This is evident in 2016 data from Express Scripts that show year-on-year price percentage shrinkage in traditional pharmaceuticals and a slowing, mid-single-digit percentage increase for specialty drugs.

Importantly, utilization growth rates are greater than unit cost rises, indicating product efficacy. If the drugs weren’t effective, doctors wouldn’t prescribe them. Assuming buyers will pay for efficacious drugs, then the prognosis for the more innovative pharmaceutical companies is good.

Notably, several of the European drug giants with promising pipelines trade at valuation discounts to the health-care sector and to their own historical averages. Examples include Novartis AG, AstraZeneca Plc, Roche Holding AG and GlaxoSmithKline Plc. These well-managed, shareholder-friendly companies generate plenty of surplus cash to reward investors. Many of them have dividend yields at least a full percentage point in excess of the global pharmaceutical and biotech industry and well above overall equity market averages.

Famously profitable, the best-managed pharmaceutical companies should be able to offset reduced unit prices with volume growth. In their report dated January 2017, Evercore ISI analysts Umer Raffat and Akash Tewari note that most of Medicare/Medicaid spending increases are due to higher enrollment, not because of pharmaceutical costs. While total U.S. health-care spending continues to increase, the percentage attributable to prescription drugs has stayed flat, at around 10 percent.

Proposed drug pricing reforms, such as bidding, reimportation, Medicare negotiating prices and value-based pricing either already exist or have serious, likely insurmountable flaws, such as public safety. Even Medicare, the colossus of U.S. pharmaceutical buyers, probably can’t negotiate prices more favorable than under current law without being forced to restrict access, as drug demand may rise. Aging demographics imply increased drug usage over at least the next decade. The most innovative pharmaceutical companies will likely benefit, even as traditional branded drug prices fade.

Ways to play it with ETFs: The SPDR S&P International Health Care Sector ETF (IRY) has the most exposure of any ETF to international pharma companies such as Novartis AG and AstraZeneca Plc. Those companies are in the top 10 holdings. The ETF has 75 percent allocated to pharma companies, 25 percent of which are based in Switzerland. IRY comes with a fee of 0.40 percent.

has the most exposure of any ETF to international pharma companies such as Novartis AG and AstraZeneca Plc. Those companies are in the top 10 holdings. The ETF has 75 percent allocated to pharma companies, 25 percent of which are based in Switzerland. IRY comes with a fee of 0.40 percent.

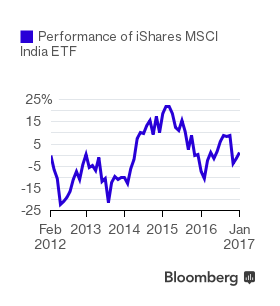

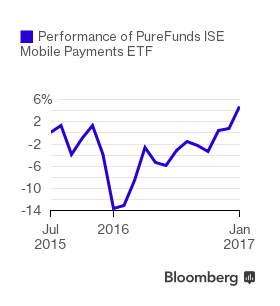

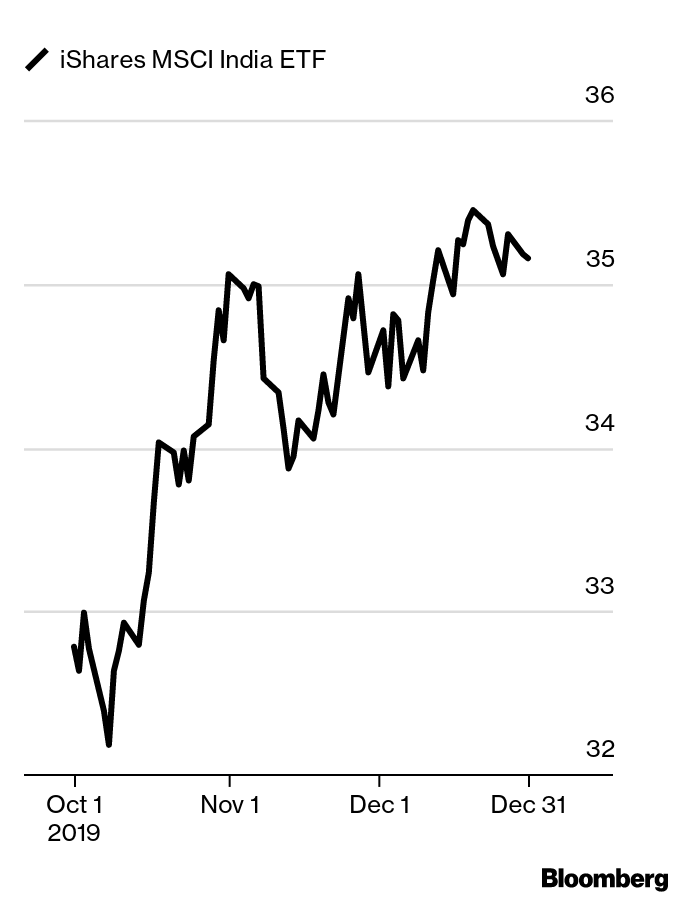

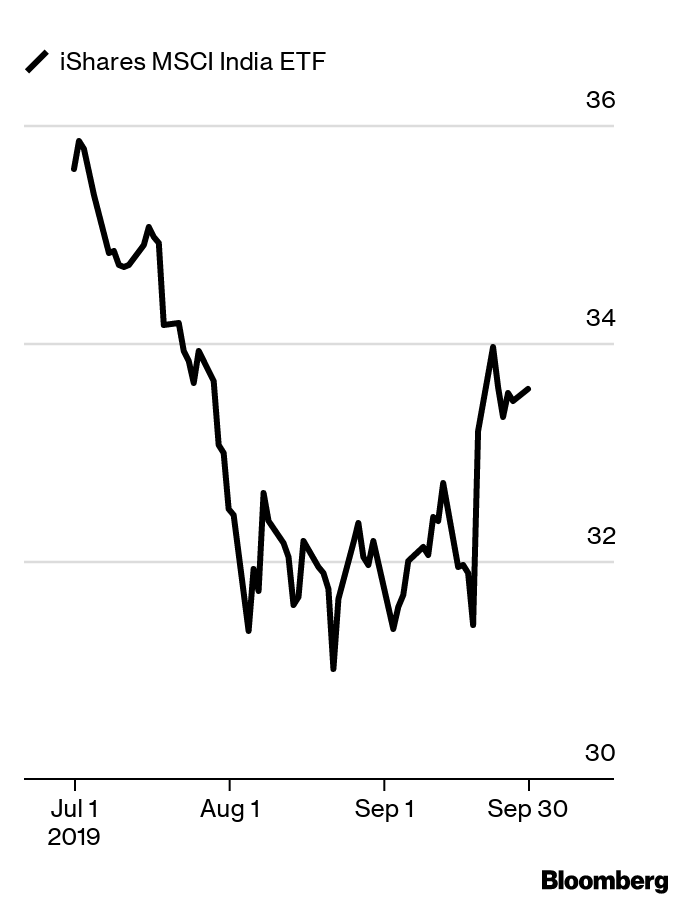

Performance of last quarter’s ETF plays: The iShares MSCI India ETF (INDA) rose 16.9 percent over the past three months. Balchunas’s other pick, the PureFunds ISE Mobile Payments ETF (IPAY)

rose 16.9 percent over the past three months. Balchunas’s other pick, the PureFunds ISE Mobile Payments ETF (IPAY) , gained 10 percent.

, gained 10 percent.

Think Long, Think Far

India is far. Flying from Los Angeles to Mumbai via Hong Kong takes about 24 hours, several meals, and almost 10,000 miles. Despite the distance, Causeway has this populous country on our investment radar. India’s demographic bulge of young consumers want to buy smartphones, cars, and homes, and their spending power rises annually.

India’s 2016 real gross domestic product growth of 7.3 percent tops the charts, beating all major countries including China. The recent demonetization to encourage a shift from cash to a digital (taxable) economy should ultimately fuel growth. Rising tax revenues facilitate fiscal spending on roads, bridges, highways, hospitals, etc., thereby boosting commerce. India’s stock market, which is severely lagging most global markets this year, has become a source of investment ideas for our clients.

Imagine a country with 90 percent of all transactions in cash. Of the roughly $240 billion of currency in circulation, the government has recently made 86 percent of that currency illegal. Exchange your soon-to-be-obsolete bank notes or they become worthless. A shortage of legal tender has placed severe working-capital constraints on businesses and harmed roughly half the population without a bank account.

Poorly implemented, the demonetization has dragged on the country’s economy as the banking system could not meet the demands of cash distribution. Longer term, the formal, taxable economy should prosper, and the central and state governments can proceed with much-needed infrastructure projects. The payment and growth inefficiencies of a cash economy should lessen.

We expect the population to open hundreds of millions of new bank accounts, resulting in a lower overall cost of funding for the country’s banking system. Prime Minister Modi’s demonetization offers India an opportunity to leapfrog several banking stages, avoiding checks and bank cards and moving directly to digital payments. We believe non-cash transactions should grow 50 percent annually through to 2025 and account for 40 percent of payment transactions. Banks that already have scale in credit and debit cards, point of sale, and mobile banking should see a substantial pickup in market share.

Way to play it with ETFs: The iShares MSCI India ETF (INDA) is the fastest growing and cheapest of the India ETFs, with an expense ratio of 0.68 percent. There is an ETF that specifically tracks the move to mobile payments, called the PureFunds ISE Mobile Payments ETF (IPAY) , but it holds 80 percent of assets in U.S. companies, with just a dash of international exposure. It’s also a little expensive, with a fee of 0.75 percent, and doesn’t trade a lot, so potential buyers should use a limit order that specifies the price they want to pay.

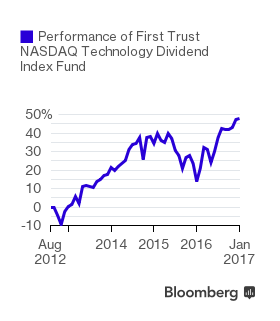

Performance of last quarter’s ETF plays: The ETF Balchunas chose to track Ketterer’s advice back in October was First Trust NASDAQ Technology Dividend Index Fund (TDIV)  . It rose 3.6 percent for the three months ended Dec 31.

. It rose 3.6 percent for the three months ended Dec 31.

Invest in Corporate ‘Self-Help’

In this seemingly endless environment of economic stagnation, what will drive revenue and profit growth? Central banks may be running out of monetary solutions to stimulate credit and demand. While we wait for the political landscape to become less muddled, investors can get access to companies engaged in operational restructuring or “self-help.”

These companies, boasting strong balance sheets and modest levels of debt, typically have managements committed to a continuous and inexorable process of cost cutting and increased efficiency. In mobile telephony, especially in Japan, China, and South Korea, several of the largest listed companies have found increasingly ingenious ways to extract above-industry-average returns from the mature telecommunications market. [China Mobile Ltd. and SK Telecom Co. Ltd. were in the top 15 holdings of the Causeway International Value Fund (CIVIX), as of June 30.] Smart self-help moves by senior managements of these companies have led to a reduction in capital expenditures and operating costs.

These companies are typically creating innovative and value-added services, introducing popular data plans and benefiting from supportive local regulations. Similarly, in the more mature segment of technology, “legacy tech” companies also have managements committed to reinvigorating growth. Even though these companies have valuable proprietary technology, sell-side analysts put some of them in the dinosaur category. But the analysts often take a short-term view. Market pessimism can give investors a chance to buy world-class technology franchises in transition.

For example, large enterprise software companies must make a successful transition from an on-premises licensing business model to a cloud-computing subscription-based model. Semiconductor companies currently expert in mobile wireless technology are making measurable progress to deliver next-generation technology. Look for efficient operations, focused and shareholder-friendly managements, as well as inherent advantages in research and development expertise and resulting defendable intellectual property. [SAP and Samsung Electronics are CIVIX holdings.]

Economic malaise aside, these great companies, albeit often labeled mature and in transition, still trade at valuations that imply the potential for above-market returns.

Way to play it with ETFs: The First Trust NASDAQ Technology Dividend Index Fund (TDIV)  holds tech companies that pay the highest dividend, which means it has the largest percentage of “legacy tech” names such as Intel Corp., Microsoft Corp., Cisco Systems Inc., and Oracle Corp. This “I love the 90s” portfolio has the lowest volatility, lowest average price-to-earnings ratio, and highest dividend yield of the technology ETFs.

holds tech companies that pay the highest dividend, which means it has the largest percentage of “legacy tech” names such as Intel Corp., Microsoft Corp., Cisco Systems Inc., and Oracle Corp. This “I love the 90s” portfolio has the lowest volatility, lowest average price-to-earnings ratio, and highest dividend yield of the technology ETFs.

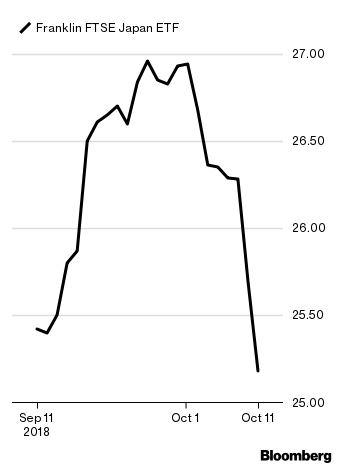

Performance of last quarter’s ETF plays: The ETF Balchunas chose to track Ketterer’s advice back in June was The WisdomTree Japan Hedged Equity Fund (DXJ)  . It rose 11 percent for the three months ended Sept. 30.

. It rose 11 percent for the three months ended Sept. 30.

Play Japan

Something interesting is happening in the Land of the Rising Sun. The Japanese equity market has slipped 20 percent from its five-year high, reached last August, reflecting an economy unresponsive to monetary stimulus. Despite this gloom, many Japanese companies have the financial wherewithal to reward shareholders with dividends.

As of late May, over 200 Japanese stocks with market caps above $1 billion also have dividend yields greater than 2 percent (several offer yields of 4 percent), with dividend payout ratios less than 50 percent. In other words, these dividends should be well covered by earnings, and (thanks to the low payout ratios) have room to grow.

Some of the best-managed companies with generous dividends include Sumitomo Mitsui Financial Group Inc. (4 percent yield), Japan Airlines Co. (3 percent), Komatsu Ltd. (3 percent), KDDI Corp., and Hitachi Ltd. (both 2.5 percent). Bonds can’t compete. The 10-year Japanese government bond yield is negative, making generous dividends all the more appealing.

In the U.S., investor demand for high-dividend-yielding stocks, and exchange-traded funds that track such stocks, has risen sharply in our own prolonged low-interest-rate environment. Perhaps the same will happen in Japan. Mrs. Watanabe, the proverbial Japanese retail investor, wants income. It may make sense to own some of these income-generating, better-quality Japanese stocks before she does.

Ways to play it with ETFs: The WisdomTree Japan Hedged Equity Fund (DXJ)  goes long the stocks mentioned by Ketterer, and many more, said Balchunas. It also shorts—bets against—the yen, and weights stocks by the size of their dividend. It yields 3 percent.

goes long the stocks mentioned by Ketterer, and many more, said Balchunas. It also shorts—bets against—the yen, and weights stocks by the size of their dividend. It yields 3 percent.

Terri Spath

Chief investment officer, Sierra Mutual Funds

Look Abroad

Volatility has become a staple of 2020, and wild swings are unnerving — but that’s not necessarily a bad thing.

This year has tested investor resolve like rarely before. Fear and uncertainty associated with the pandemic sent investors fleeing everything from tech stocks to municipal bonds, and the quickest bear market decline in history was followed by the fastest rally on record early in the year.

Whether you are looking to diversify or for new avenues of growth, international stocks are the answer. The prospect of accelerating growth over the long term, increasing productivity, and growing standards of living support a thesis that the world’s strongest advance will come outside U.S. borders.

A weakening U.S. dollar also gives life to foreign stocks. Research shows that in the years when the American currency is relatively weak, shares abroad go up 85% of the time.

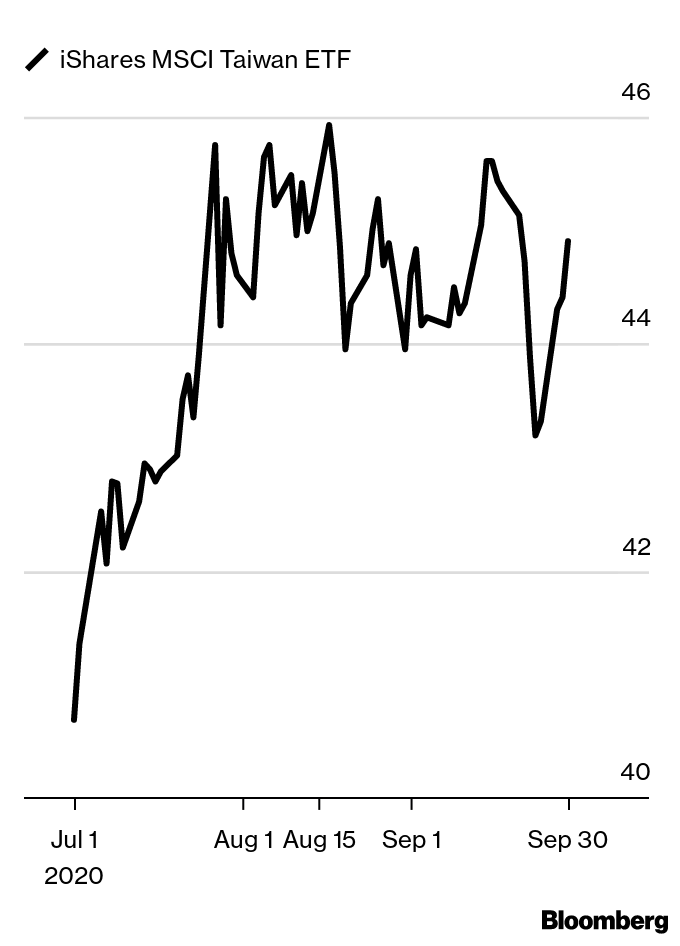

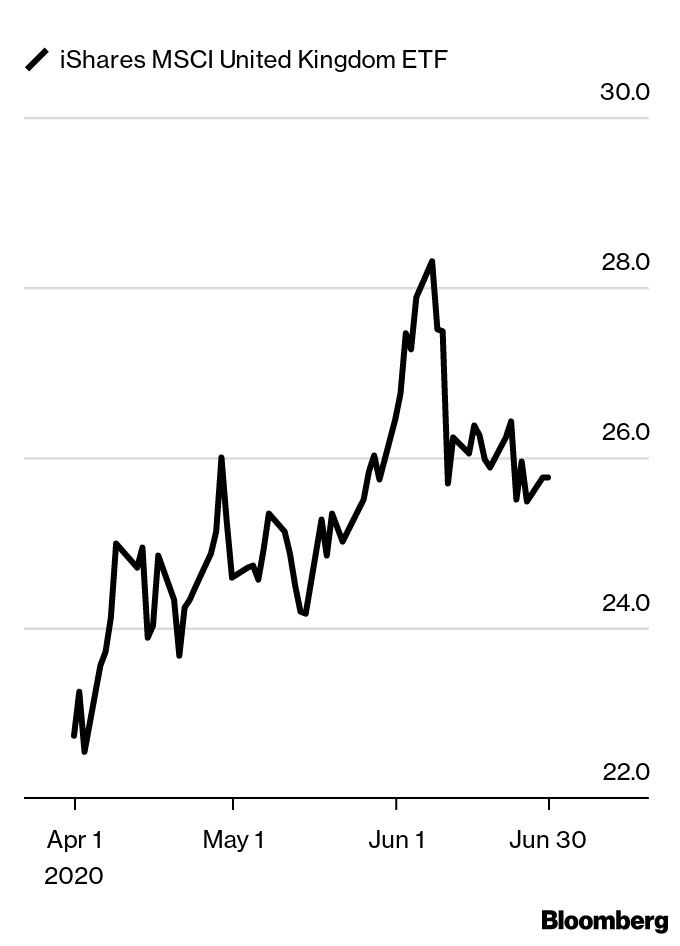

Broadly, the iShares MSCI Emerging Markets ETF (EEM) tracks over 800 large- and mid-sized companies in China, Taiwan, Korea, India and more. We recommend going a step further and focusing on exposure to Taiwan via iShares MSCI Taiwan ETF (EWT) and India via WisdomTree Indian Earnings Fund (EPI). These two countries offer terrific demographics and the ETFs participate in ample exposure to technology companies. Strong growth and favorable industry exposure combine for promising opportunities for investors.

How to play it with ETFs: Even after a relatively strong first half, the iShare MSCI Taiwan ETF (EWT) could have room to run. Its 12-month forward earnings-per-share growth, led by cyclical stocks, is north of 23% on 9.7% sales growth, according to Bloomberg consensus estimates. The expense ratio is 0.59%.

could have room to run. Its 12-month forward earnings-per-share growth, led by cyclical stocks, is north of 23% on 9.7% sales growth, according to Bloomberg consensus estimates. The expense ratio is 0.59%.

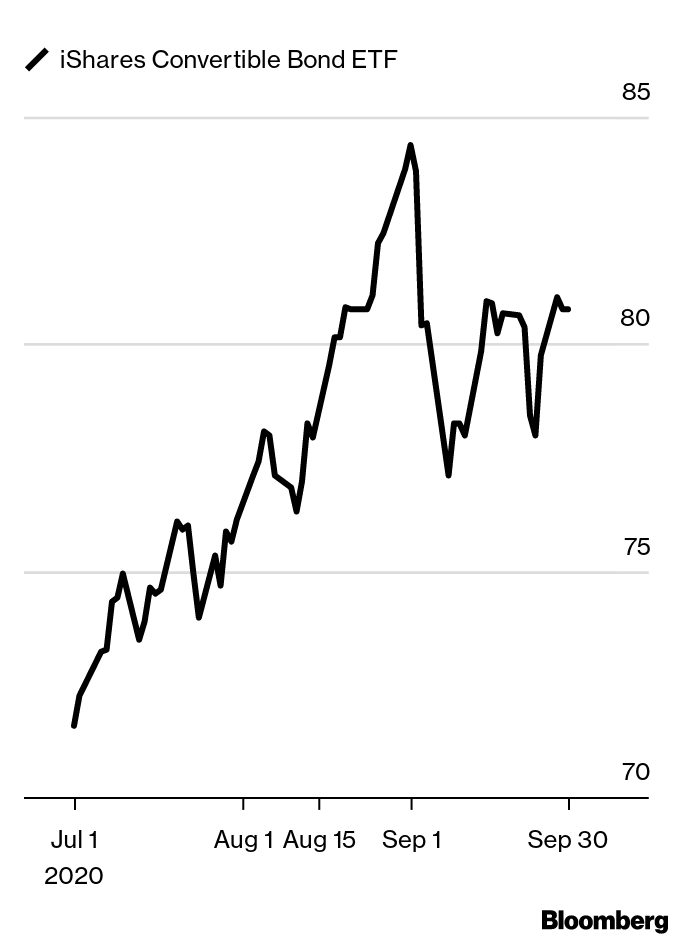

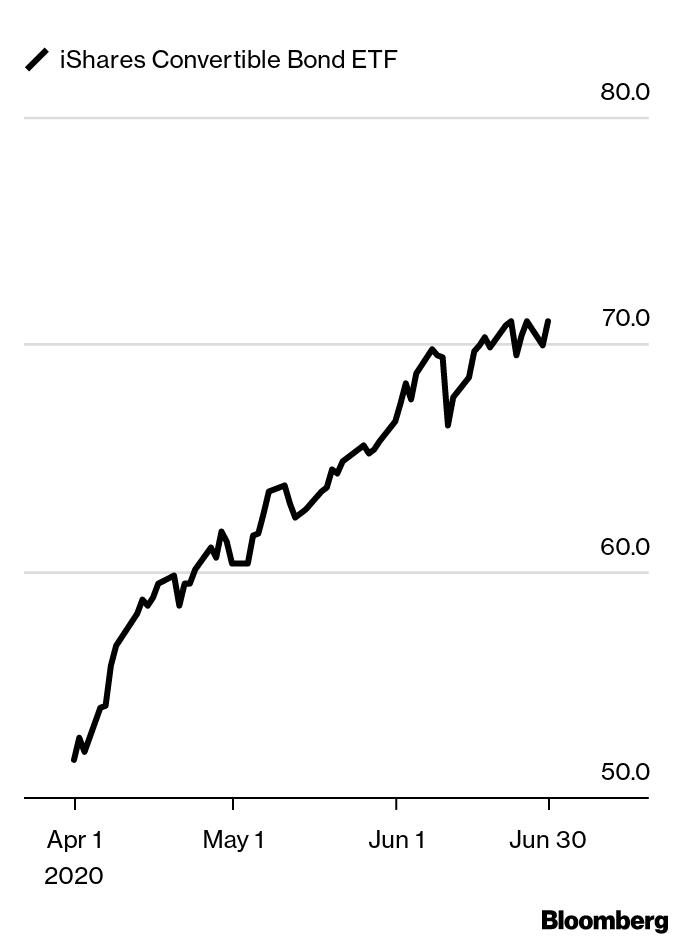

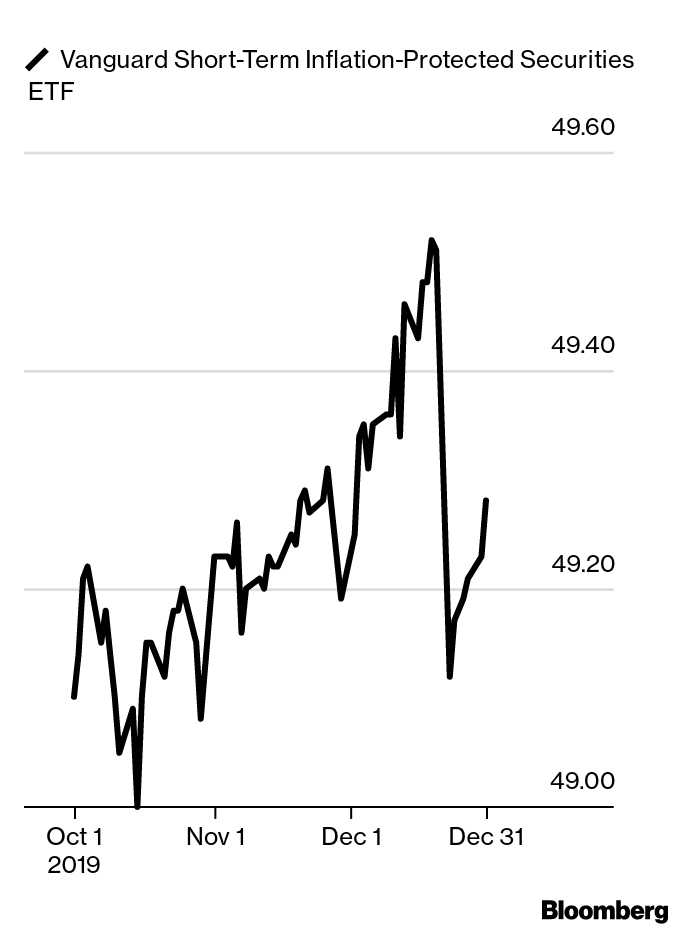

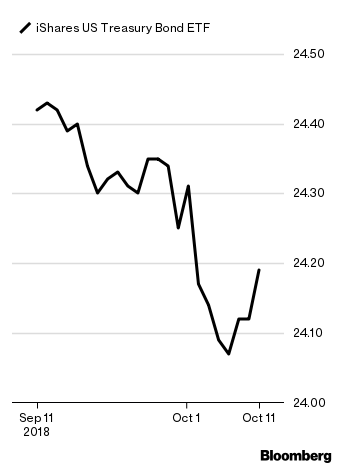

Performance of last quarter’s ETF plays: The iShares Convertible Bond ETF (ICVT) rose 15%.

rose 15%.

Hop Into a Convertible

The Federal Reserve has said that it will do whatever it takes, igniting a stampede into stocks. The most common question we have fielded recently is why the S&P 500 has recovered to January 2020 levels when economic growth has contracted, millions are out of work and default rates are surging. The economic data is awful, but the Fed has proclaimed that the printing presses are rolling and they are ready for a shopping spree.

The disconnect presents a perfect storm. The sharp snapback in recent months increases the probability of volatility and painful losses in the future. To play defense, we see convertible bond funds as a good place to put $10,000 now. These are bonds that can be converted into stock at a specific price.

Historically, convertibles have offered equity sensitivity on the upside while cushioning downside risk by paying income. Getting exposure through a mutual fund gives diversification as well as access to potential alpha created by the portfolio manager. We recommend several opportunities in the convertible bond universe. Top picks are Columbia Convertible Securities Fund (PACIX) and Calamos Convertible Fund (CCVIX). There is also an iShares Convertible ETF (ICVT) for investors that prefer using ETFs.

How to play it with ETFs: Balchunas also points to the iShares Convertible Bond ETF (ICVT) , which has an expense ratio of 0.20%. The fund has over 38% in software and internet companies, darlings of this year’s rally.

, which has an expense ratio of 0.20%. The fund has over 38% in software and internet companies, darlings of this year’s rally.

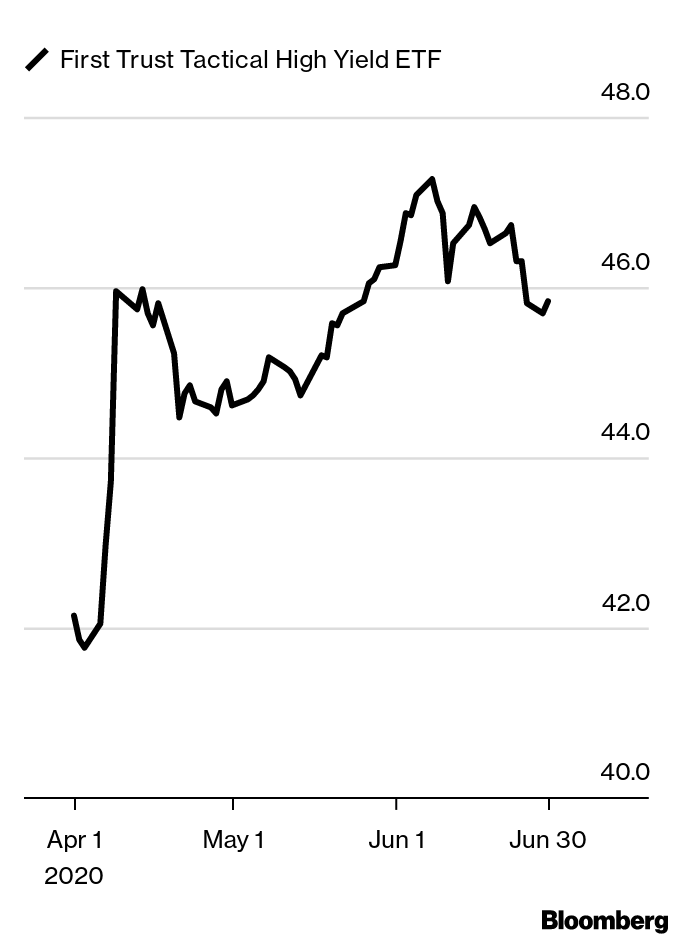

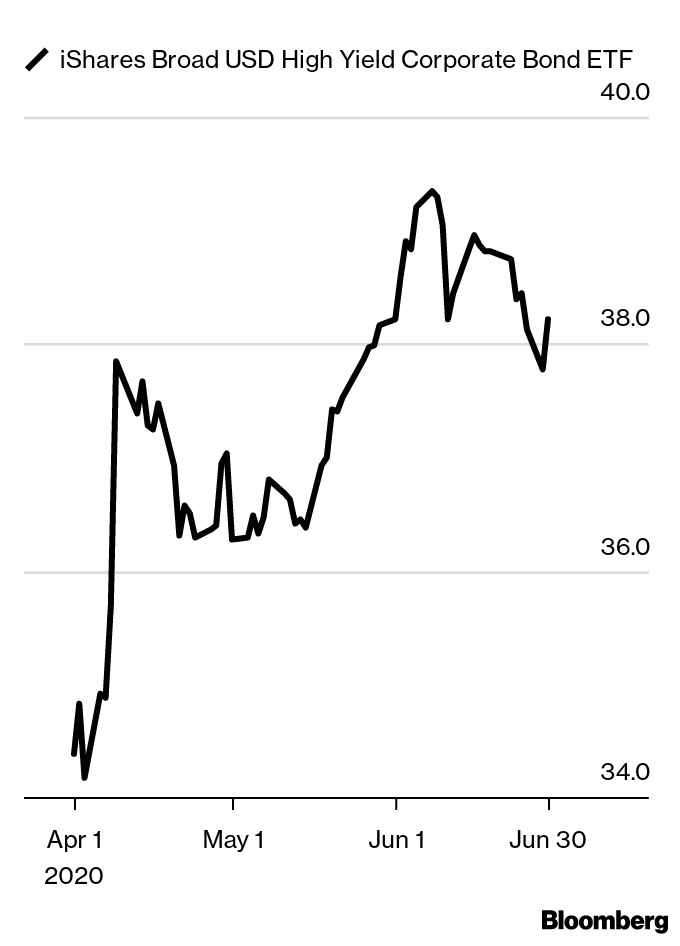

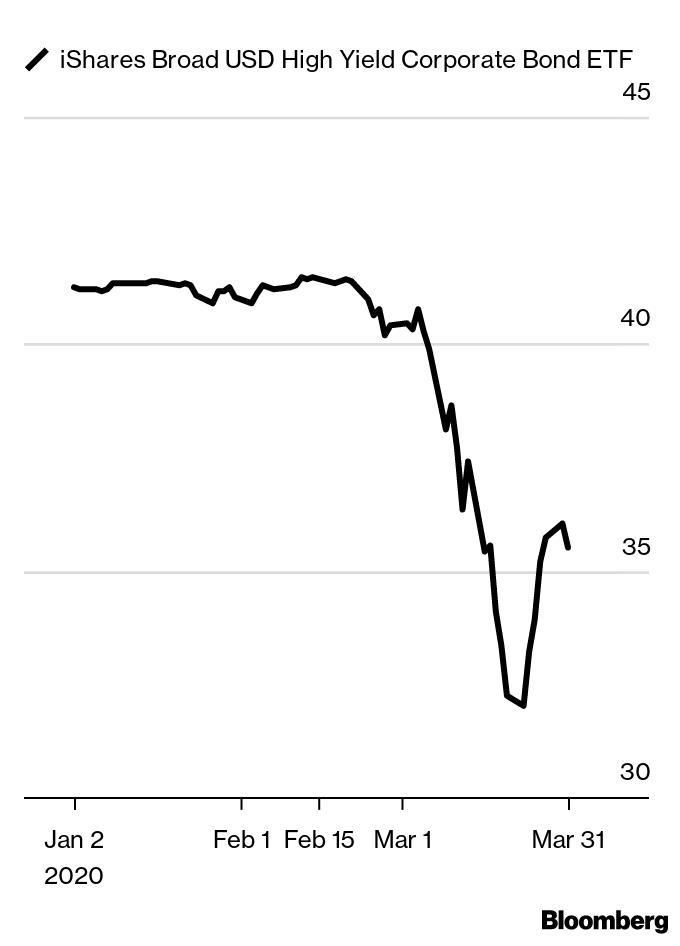

Performance of last quarter’s ETF plays: The First Trust Tactical High Yield ETF (HYLS) and the iShares Broad USD High Yield Corporate Bond ETF (USHY)

and the iShares Broad USD High Yield Corporate Bond ETF (USHY) saw gains of 6.4% and 7.9%, respectively.

saw gains of 6.4% and 7.9%, respectively.

Look to High Yield

Like a black swan flying against a dark night sky, the Covid-19 virus arrived without much warning, affecting our personal and financial lives. The impact on nearly every asset class available was swift and brutal. The optimism that defined the start of a new decade quickly cycled to anxiety, denial and outright fear. While cities, states and the U.S. government issued stringent health guidelines, the Federal Reserve and Trump Administration committed to massive action to steady financial markets and the economy.

It is exactly in times like these where the question “Where to put $10,000?” seems like it deserves an answer of “Under the mattress!”

So we ask the same question a bit differently: When it comes time to buy, will you do it?

Panic is not a strategy. Hope is also not a strategy. Maximum financial opportunity coincides with maximum pessimism, according to legendary investor Sir John Templeton.

High-yield corporate bond spreads over comparable maturity U.S. Treasury bonds have widened to levels that historically have translated into great opportunity for investors with a medium- to long-term investment horizon. Investors in high yield are getting paid well for the risk taken over a “risk-free” U.S. bond issue.

Risk matters, and it is intriguing to know that in past periods of fear when high-yield corporate bonds have offered similar returns, the asset class has rebounded more quickly and outpaced U.S. stocks in the following months and even up to three years.

In a period when active management is more likely to outpace passive benchmarks, our top mutual fund picks are two Diamond Hill funds: Corporate Credit Fund (DHSTX) and High Yield Fund (DHHIX). We also like PIMCO’s High Yield Fund (PHYRX) for its recent rebound. After drawdowns in March, these funds are poised to gain with less risk than stocks and similar returns.

How to play it with ETFs: First Trust Tactical High Yield ETF (HYLS) is an actively managed corporate high yield fund that has shown a better late March rebound than the iBoxx Liquid High Yield index. The $1.2 billion fund can have short positions for up to 30% of net assets and long positions up to 130%, opportunistically, with the ability to earn return on the short side. The fund charges 95 basis points. Alternatively, the iShares Broad USD High Yield Corporate Bond ETF (USHY)

is an actively managed corporate high yield fund that has shown a better late March rebound than the iBoxx Liquid High Yield index. The $1.2 billion fund can have short positions for up to 30% of net assets and long positions up to 130%, opportunistically, with the ability to earn return on the short side. The fund charges 95 basis points. Alternatively, the iShares Broad USD High Yield Corporate Bond ETF (USHY) is a cheap-and-deep passive alternative holding 1,700 junk bonds and charging 0.15%.

is a cheap-and-deep passive alternative holding 1,700 junk bonds and charging 0.15%.

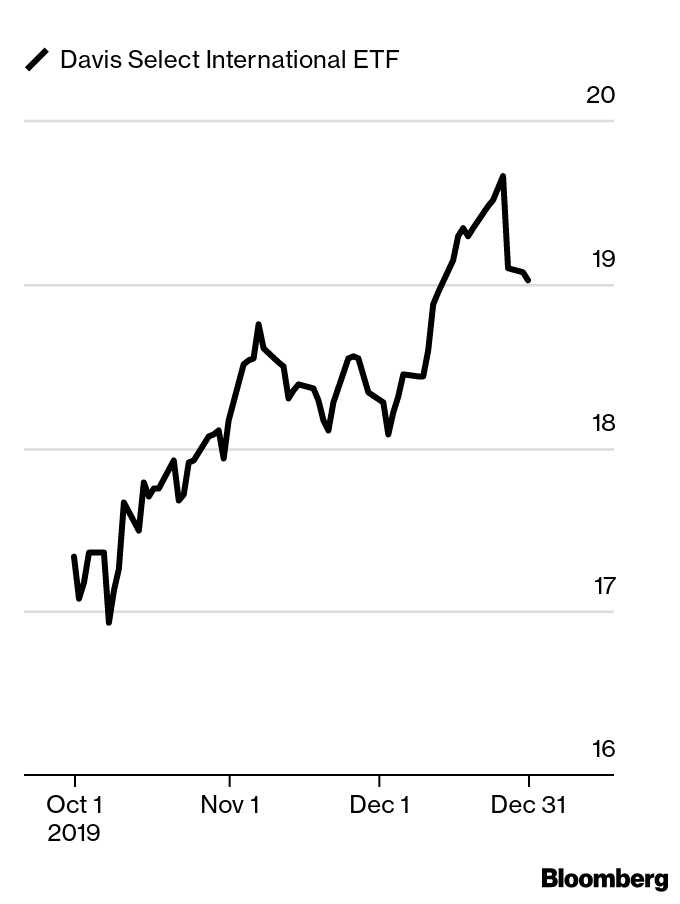

Performance of last quarter’s ETF plays: The Davis Select International ETF (DINT) saw a price drop of 21.7%.

saw a price drop of 21.7%.

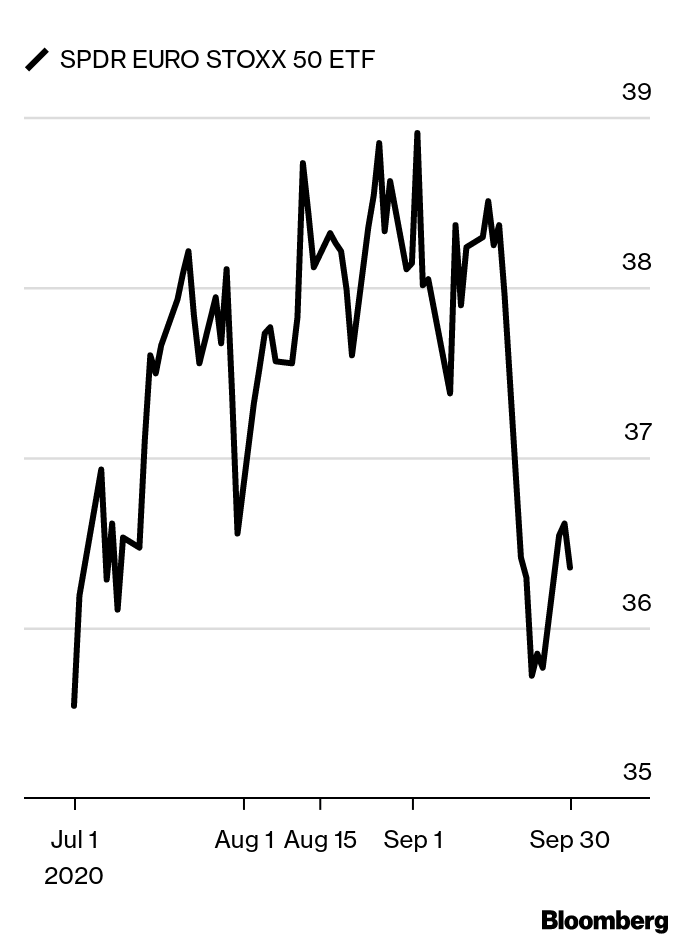

Take Your Money Abroad

After a decade of relative underperformance, international stocks are staging a stealth rally and mark our top pick for new money. International stocks offer diversification to a domestically dominated stock portfolio, but that’s not the main reason why we recommend readers put their $10,000 to work outside U.S. borders. Recently, we’ve seen stronger uptrends in international stocks than for domestic ones and the risk, as measured by historic volatility, is similar. We see this as promising and recommend investors pay attention to opportunities abroad.

Last year, nothing seemed to move global equities markets more often or with more tenacity than headlines renewing optimism or pessimism around U.S. and China trade talks. The Phase One U.S.-China deal in December propelled a late-year spike in global stocks and a banner year for global equities.

While trade challenges still exist, the needle is moving in the right direction and a resulting rebound in global economic growth would benefit international stocks. Further, systematic fiscal stimulus overseas is lurking on the horizon. Relative valuations are also low and can therefore offer more upside potential (and less downside risk).

While geographic diversification is generally a beneficial tactic, we warn against using passive benchmark-hugging exchange-traded funds. International stocks are an asset class where actively managed fund managers can consistently demonstrate alpha, or better risk-adjusted performance relative to a benchmark. A top pick of ours is Artisan Global Opportunities (ARTRX).

How to play it with ETFs: For those looking for that active approach, Balchunas says a steadily growing option is the Davis Select International ETF (DINT) , which tracks a 31-stock basket of the manager’s best picks. That means there will be more volatility—which could be good or bad. It outperformed the ultra-popular ETF play in the area, the iShares Core MSCI EAFE ETF (IEFA)

, which tracks a 31-stock basket of the manager’s best picks. That means there will be more volatility—which could be good or bad. It outperformed the ultra-popular ETF play in the area, the iShares Core MSCI EAFE ETF (IEFA) , over the past 12 months. You have to pay up for DINT, as it charges 0.75% to IEFA’s 0.07%.

, over the past 12 months. You have to pay up for DINT, as it charges 0.75% to IEFA’s 0.07%.

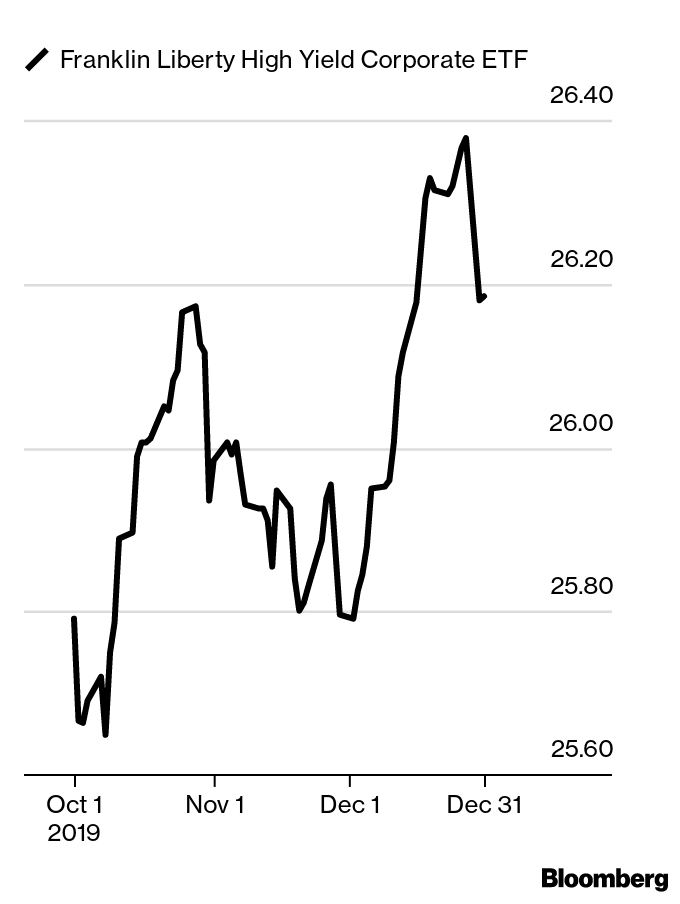

Performance of last quarter’s ETF plays: The price of the Franklin Liberty High Yield Corporate ETF (FLHY) rose 1.5% and it had a 3.1% total return for the quarter.

rose 1.5% and it had a 3.1% total return for the quarter.

Lower for Longer —Or Forever

Lower for longer is fast turning into lower forever.

Lower for longer was a phrase coined several years ago as interest rates stayed at historically low levels for longer than nearly anyone had predicted. It may be time to expect lower forever.

Here are a few facts to consider:

- Over 30% of investment-grade global debt, more than $17 trillion, bear sub-zero yields. This means that all else equal, the borrower of the debt will owe less than was originally borrowed.

- Austria recently issued 100-year debt at a 1.2% yield.

- The $27.8 trillion of non-U.S. dollar investment grade global debt is yielding 0.11%.

Here in the U.S., the yield on the 10-year Treasury is 1.53% versus 1.94% for the S&P 500. It’s as though investors are buying stocks for yield and bonds for capital appreciation (which results as interest rates fall).

Except that stocks have far worse downside risk than bonds. A favorite adage is that “a bad day in the stock market is a bad year for the bond market.” A better way to earn income in bonds with less risk than stocks is to hold high-yield corporate bond funds.

We recommend that readers with $10,000 to invest put that in an actively managed high-yield corporate bond fund. High-yield corporate bonds are kicking off as much as 6%, which is downright juicy in this “lower forever” environment. An actively managed mutual fund, or even a passive ETF such as the SPDR Bloomberg Barclays High Yield Bond ETF (JNK) or the iShares iBoxx High Yield Corporate Bond ETF (HYG) diversifies over hundreds and sometimes thousands of bonds to substantially reduce risk and the impact of any particular corporation defaulting on its obligation.

Earnings and cash flows are healthy and will support interest and bond payments for the foreseeable future. Like any investment, though, we recommend using a sell strategy to exit early when trends (inevitably) turn down. Our quantitative, rules-based approach uses banded moving averages that typically give a sell signal for lower- and medium-volatility asset classes within a few percentage points of a top price.

In a lower forever environment, economically solid high-yield corporate bond funds offer solid income with manageable risk.

How to play it with ETFs: The actively managed Franklin Liberty High Yield Corporate ETF (FLHY) is outpacing the iShares iBoxx High Yield Corporate Bond ETF (HYG)

is outpacing the iShares iBoxx High Yield Corporate Bond ETF (HYG) by nearly 180 basis points for the year to date. The fund is diversified across sectors and issuers, with nearly 82% in U.S. corporate debt. The expense ratio is 0.40%.

by nearly 180 basis points for the year to date. The fund is diversified across sectors and issuers, with nearly 82% in U.S. corporate debt. The expense ratio is 0.40%.

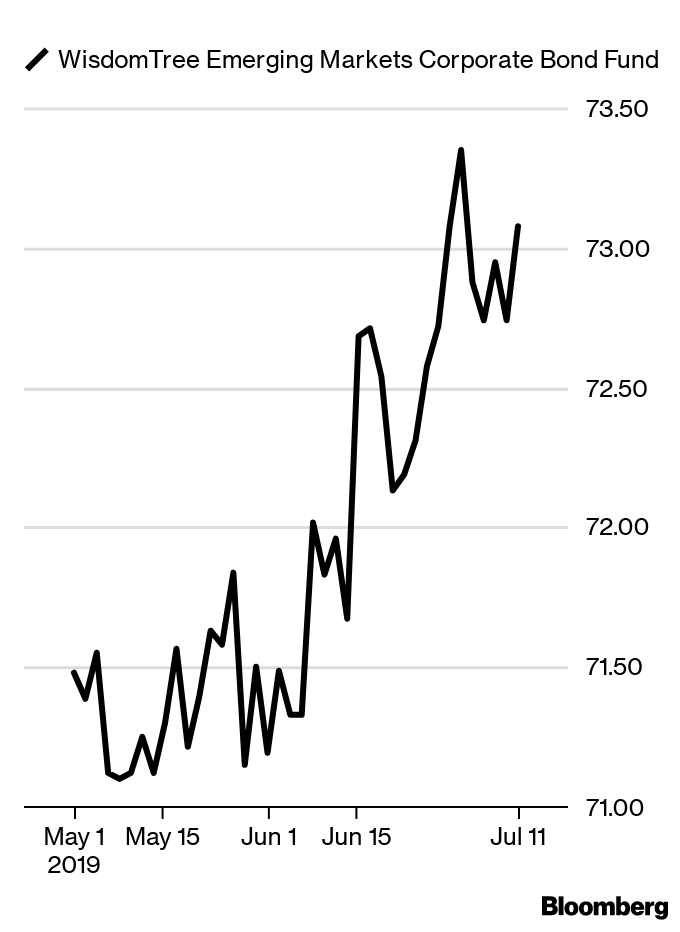

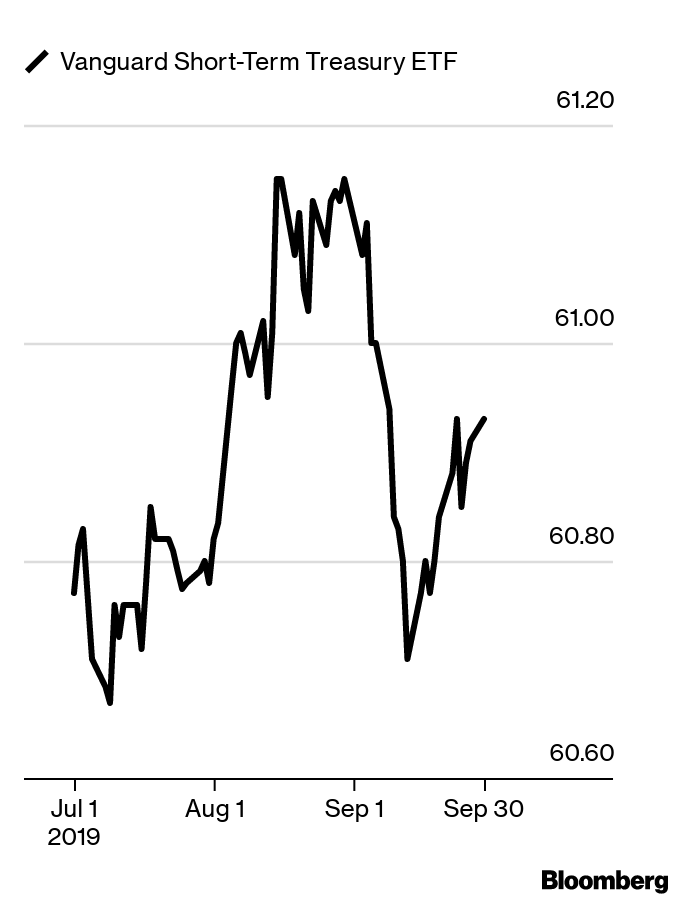

Performance of last quarter’s ETF plays: WisdomTree Emerging Markets Corporate Bond Fund (EMCB) rose 0.1% for the quarter.

rose 0.1% for the quarter.

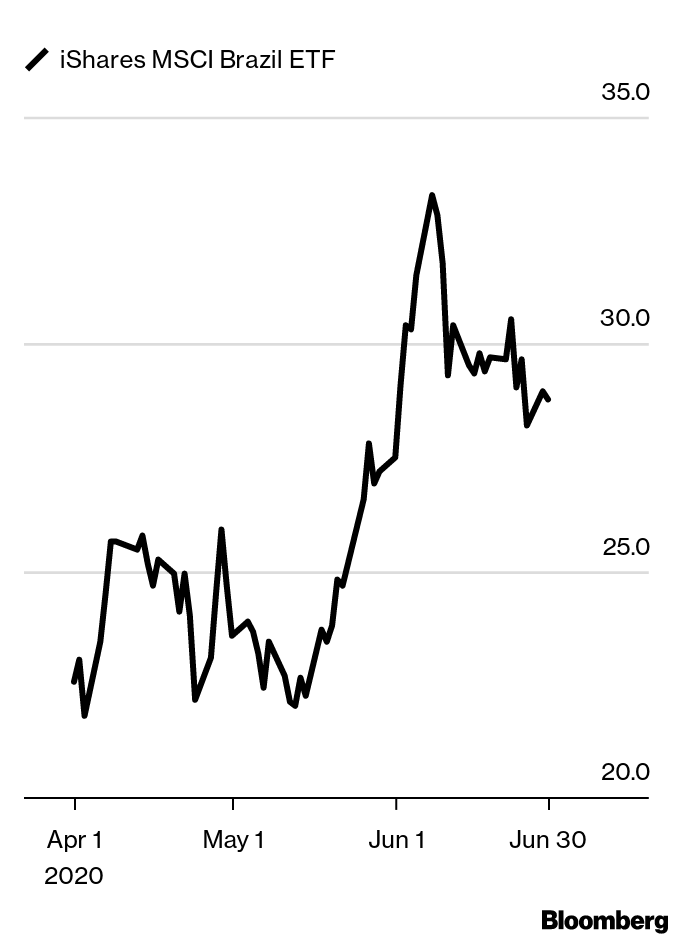

Target Emerging Market Debt

U.S. stock and bond markets are in a state of confusion. The S&P 500 and other benchmark indices for U.S. stocks are tapping on new all-time highs, anticipating a soft landing for the economy, engineered with finesse by the Federal Reserve. The U.S. bond market seems much more concerned—there is nothing normal about a 10-year Treasury bond below 2% and a 90-day Treasury bill above 2%. More daunting is that this relationship in yields has historically signaled negative economic growth in the near future.

The confusion in financial markets has, and surely will, contribute to further uncertainty and volatility. Managing volatility, or risk, is one of the few things investors can control. For these reasons, we favor emerging markets debt over emerging markets equity, and recommend that readers with $10,000 to invest put that in an actively managed emerging markets debt fund (EMD).

Why EMD? The asset class is currently, and often has been, overlooked—and it shouldn’t be. The global economy is growing, albeit at a slower rate than last year at this time, but growing. At the same time, debt-to-GDP ratios are stronger across the board for emerging countries over developed ones, a fact that has been largely missed. Also, yields for EMD funds are at least 5%, offering a built-in return if prices remain stable.

EMD also has a lower correlation to more traditional asset classes like stocks or bonds, providing strong diversification. Against a backdrop where U.S. asset classes are acting confused, EMD has delivered steady returns with low volatility. This isn’t limited to the U.S. Over the past year, emerging markets equities have lost money (based on EEM, the iShares MSCI Emerging Markets ETF) and shocked with an almost 20% drawdown. EMD is up more than 10% (based on EMB, the iShares J.P. Morgan USD Emerging Markets Bond ETF) on a generally smooth ride. More return, less risk.

The key to successful investing in EMD is to use an actively managed mutual fund. The performance of any particular developing country can be vastly different—what is impacting Russia can be very different than what is driving Turkey. An active manager can guide a portfolio more effectively than a benchmark that is required to hold the best and the worst securities. An actively managed fund will also hold hundreds of bonds, allowing far greater diversification than an individual can achieve through an individual portfolio.

Our top picks in EMD are DoubleLine Emerging Markets Fixed Income Bond fund (DBLEX) and MFS Emerging Markets Debt Fund (MEDIX). For those with a view of a weakening dollar, PIMCO Emerging Markets Local Currency and Bond Fund (PELBX) looks great.

Way to play it with ETFs: Balchunas suggests WisdomTree’s Emerging Markets Corporate Bond Fund (EMCB) , which has gained near 10% year-to-date on both income and capital appreciation from corporate issuers. The geographic exposure spans Luxembourg, Netherlands, Mexico, Turkey and India, among others. The fund has broad industry diversification and maturity range, and a 0.60% fee.

, which has gained near 10% year-to-date on both income and capital appreciation from corporate issuers. The geographic exposure spans Luxembourg, Netherlands, Mexico, Turkey and India, among others. The fund has broad industry diversification and maturity range, and a 0.60% fee.

Russ Koesterich

Portfolio manager, BlackRock Global Allocation Fund

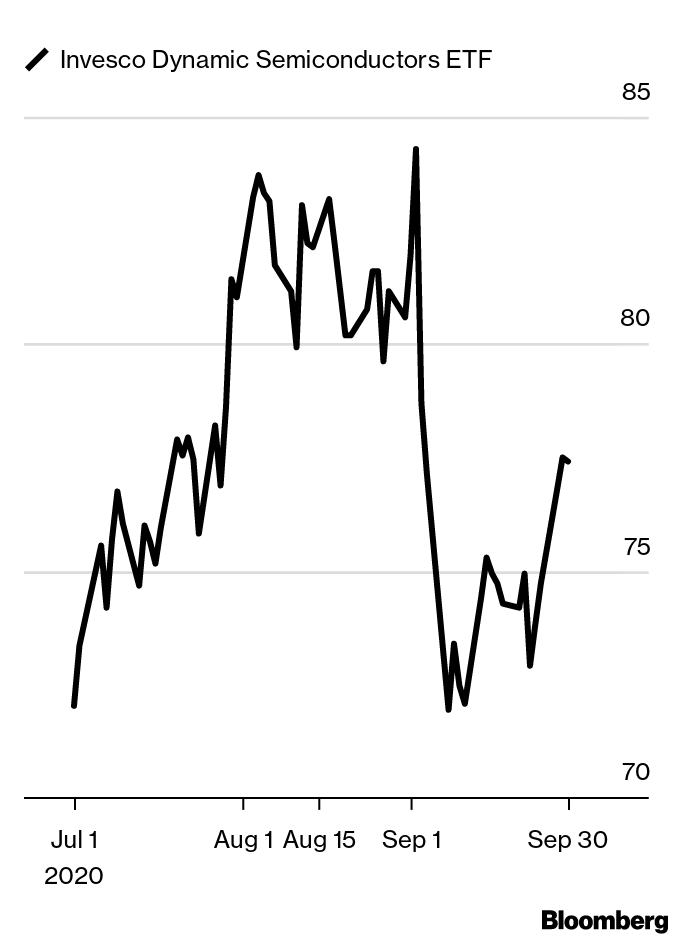

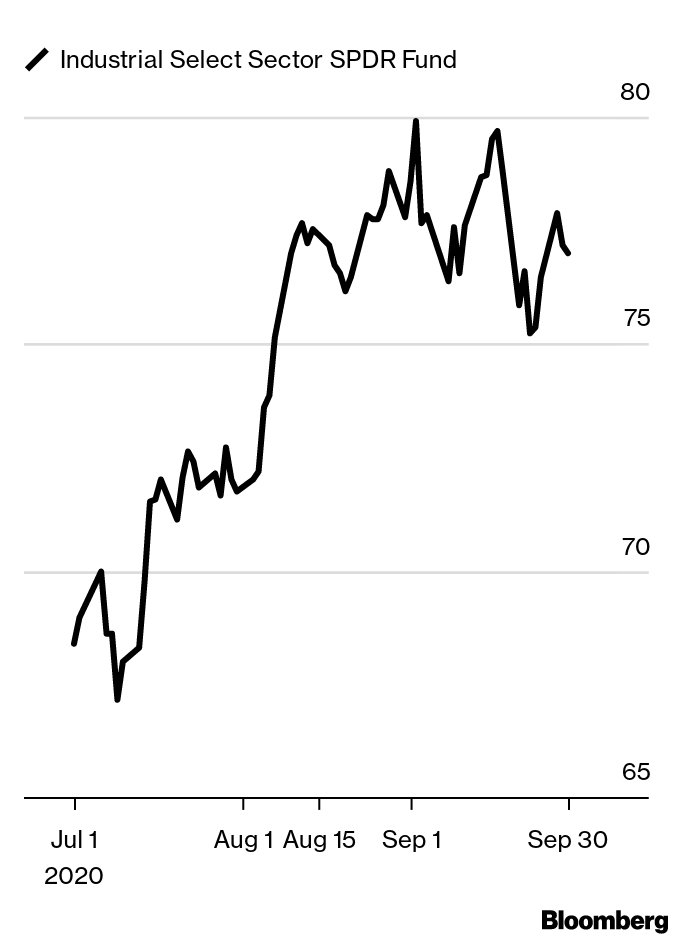

Buy High-Quality Cyclicals

After being trounced by growth stocks — such as tech companies — during both the market selloff and subsequent rebound this year, cyclical stocks are starting to have their day. There are at least two arguments for rotating into them: The economy is doing much better than expected, and these shares are playing catch-up with the rest of the market.

In recent months, economic data has been exceeding expectations by the largest margin in at least a decade. Economic improvement provides a catalyst for closing a yawning performance gap. For the year-to-date, the S&P 500 is up 3.6%, while tech stocks have gained about 26%. By contrast, shares of industrial companies are down more than 4%.

When thinking about adding cyclicals, emphasize quality, not deep value. Remain leery of piling into secularly challenged industries — whose long-term growth are uncertain — such as energy. Instead, focus on niche areas with long-term pricing power, such as rails and specialty chemicals. Another way to play the theme is to focus on areas where cyclical and secular growth intersect, such as semiconductors.

The lesson here is to be discerning. A recovering economy supports cyclicals, but emphasize companies with earnings consistency and high profitability.

How to play it with ETFs: Balchunas suggests the Invesco Dynamic Semiconductors ETF (PSI) . It caps holdings at 30 semiconductor producers and adjusts them using fundamental quality and momentum criteria. The expense ratio is 0.61%.

. It caps holdings at 30 semiconductor producers and adjusts them using fundamental quality and momentum criteria. The expense ratio is 0.61%.

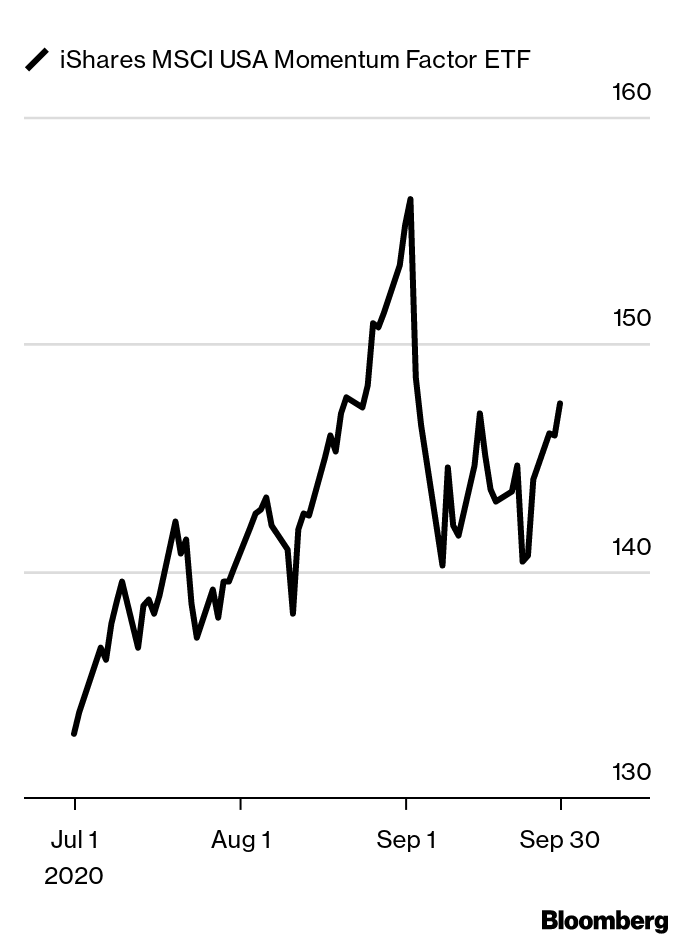

Performance of last quarter’s ETF plays: Balchunas’ suggestion, the iShares MSCI USA Momentum Factor ETF (MTUM) , was up 12.4% in the third quarter.

, was up 12.4% in the third quarter.

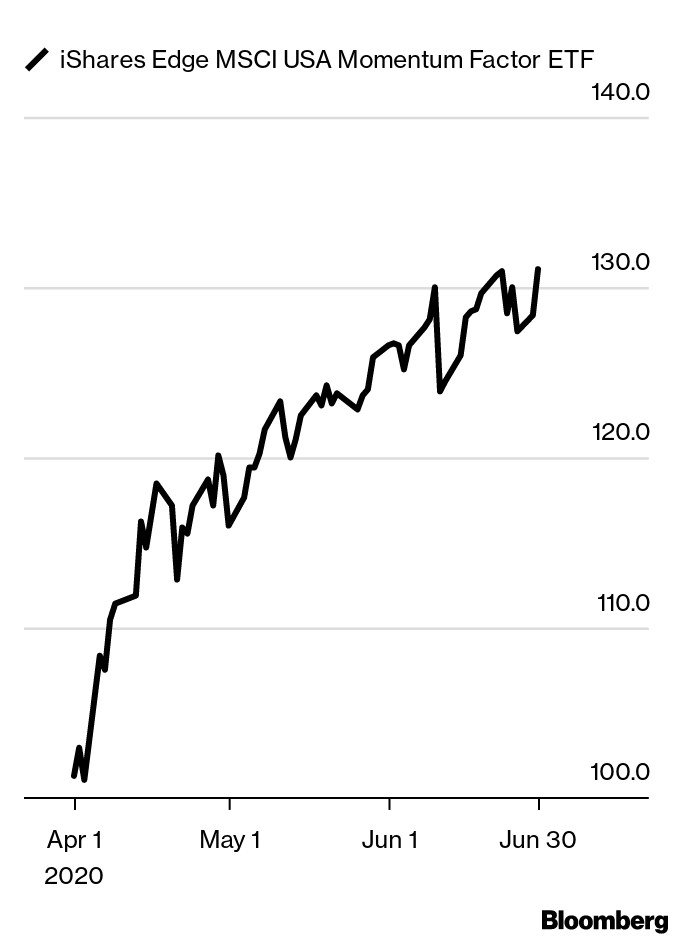

Go With the Flow

Even as the pandemic subsides, both unemployment and savings are likely to remain elevated, and value investing — where you focus on beaten-down assets seen as relative bargains — is likely to struggle. Value-style investing typically works at the bottom, because investors anticipate a strong recovery on the back of pent-up demand. Today, circumstances are very different, with a lot of uncertainty and what’s likely to be an uneven recovery.

But momentum investing — or following an existing market trend — is likely to thrive, as it benefits from the policy reaction to volatility: more liquidity. Historically, rapid growth in liquidity has favored momentum, particularly compared with strategies like value investing.

While the long-term impact of the Covid-19 pandemic is hard to predict, it is not difficult to imagine an acceleration in trends that were already evident prior to the crisis: internet commerce, cloud computing, social media and more time and money spent online.

Most momentum portfolios or funds are overweight industries that aren’t affected too much by short-term factors: technology and increasingly healthcare, specifically biotech. To the extent these segments are more insulated, and in some cases stand to benefit from longer-term structural changes, this may further favor the style.

How to play it with ETFs: Balchunas suggests the iShares Edge MSCI USA Momentum Factor ETF (MTUM) , which holds some of the largest tech companies. The ETF caps each position at 5%, so may book gains as the big get bigger. The expense ratio is 0.15%.

, which holds some of the largest tech companies. The ETF caps each position at 5%, so may book gains as the big get bigger. The expense ratio is 0.15%.

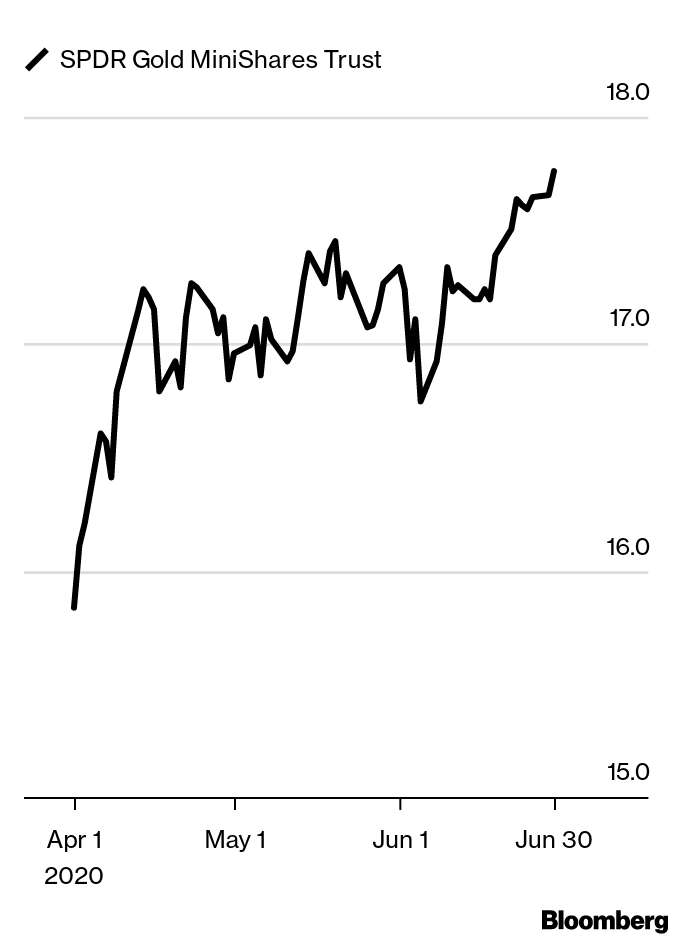

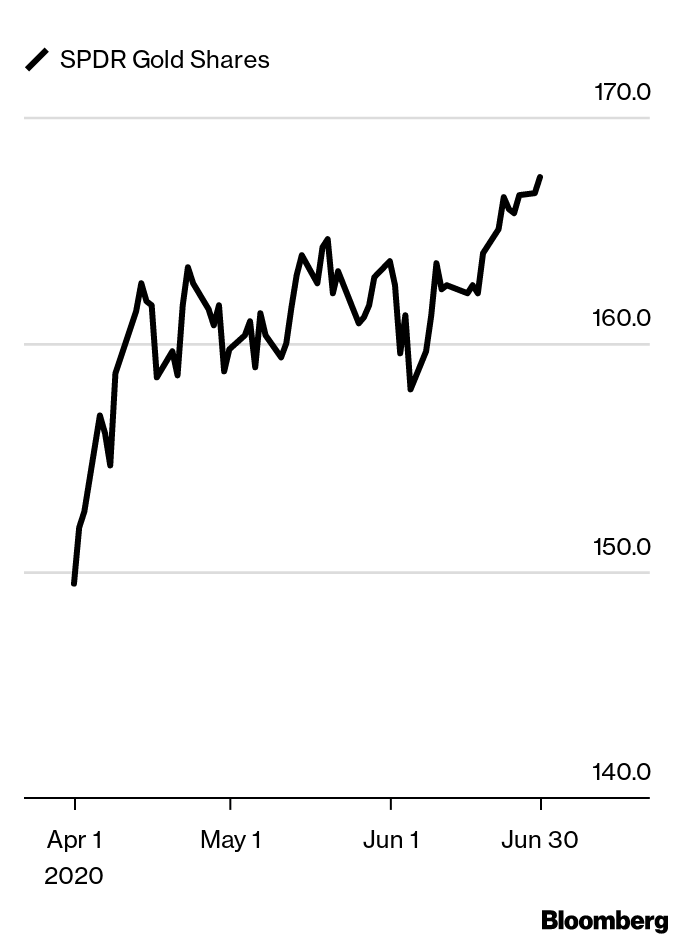

Performance of last quarter’s ETF plays: The SPDR Gold MiniShares Trust (GLDM) and SPDR Gold Shares (GLD)

and SPDR Gold Shares (GLD) both rose 9.8%.

both rose 9.8%.

Insulate with Gold

Given the human and economic toll that the Covid-19 virus has already extracted, it’s not surprising that just five major asset classes posted gains in the first quarter. Apart from classic safe havens — U.S. Treasuries and German Bunds — the list includes two currencies — the yen and the U.S. dollar — as well as gold.

While we can only hope that the second quarter is less painful than the first, investors need to continue to look for ways to insulate portfolios even as they start to venture back into stocks. While no hedge works in all circumstances, given the current combination of record central bank stimulus, a rapid and unprecedented drop in economic activity and negative real interest rates, investors should look to increase exposure to gold.

With all central bank interest rates at or near zero, the dollar is likely to be contained. After initially surging on foreign demand, the dollar has pulled back into its long-term range. This is important as gold’s efficacy as a hedge is partly a function of the dollar. Gold tends to perform best when the dollar is flat-to-down.

Growth expectations are collapsing, and while often viewed as an inflation hedge, gold performs best when investors are worried about too little growth. Historically, gold has risen the fastest when forward-looking economic measures, such as manufacturing surveys, are falling rapidly. This is exactly the situation we’re in today.

Real (inflation-adjusted) interest rates are negative and likely to stay that way. As an asset class that produces no income, gold typically suffers when real rates are high. In these environments, investors sell gold as they’re unwilling to forego the opportunity cost of lost income. Today we have the exact opposite: U.S 10-year real yields are -0.30%, down roughly 0.90% in barely a month. In an environment in which bond yields are close to zero, and decidedly negative after inflation, there is no opportunity cost to holding gold.

How to play it with ETFs: Balchunas points to the SPDR Gold MiniShares Trust (GLDM) as a way to gain exposure to the price of gold in a lower-cost ETF designed for retail investors. Its 18-basis point expense ratio is less than half that of SPDR Gold Shares (GLD)

as a way to gain exposure to the price of gold in a lower-cost ETF designed for retail investors. Its 18-basis point expense ratio is less than half that of SPDR Gold Shares (GLD) , which commands a higher fee for the liquidity it offers institutional investors. GLDM has $1.8 billion in assets.

, which commands a higher fee for the liquidity it offers institutional investors. GLDM has $1.8 billion in assets.

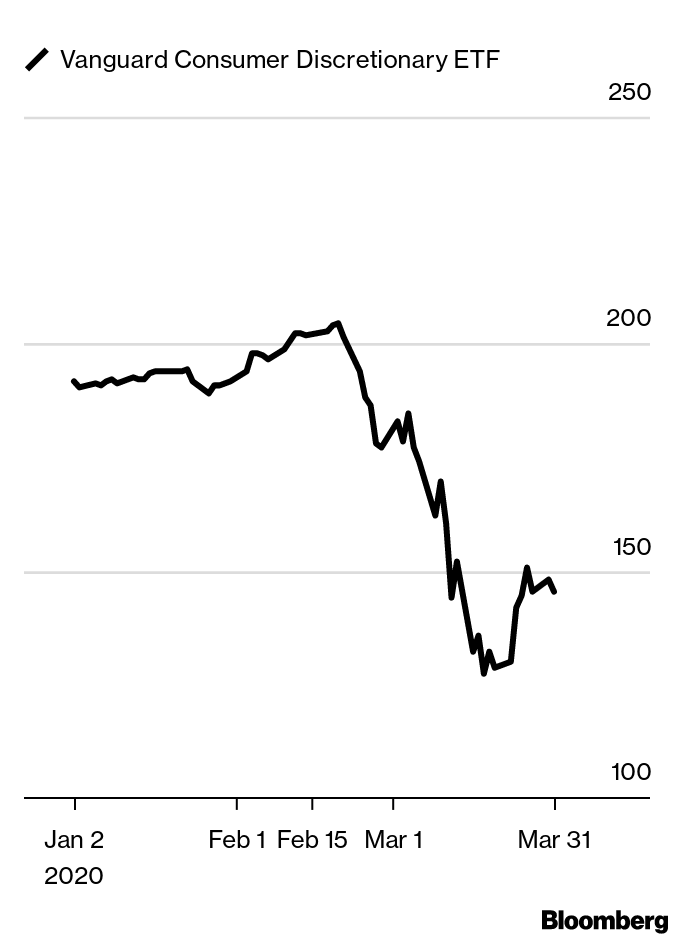

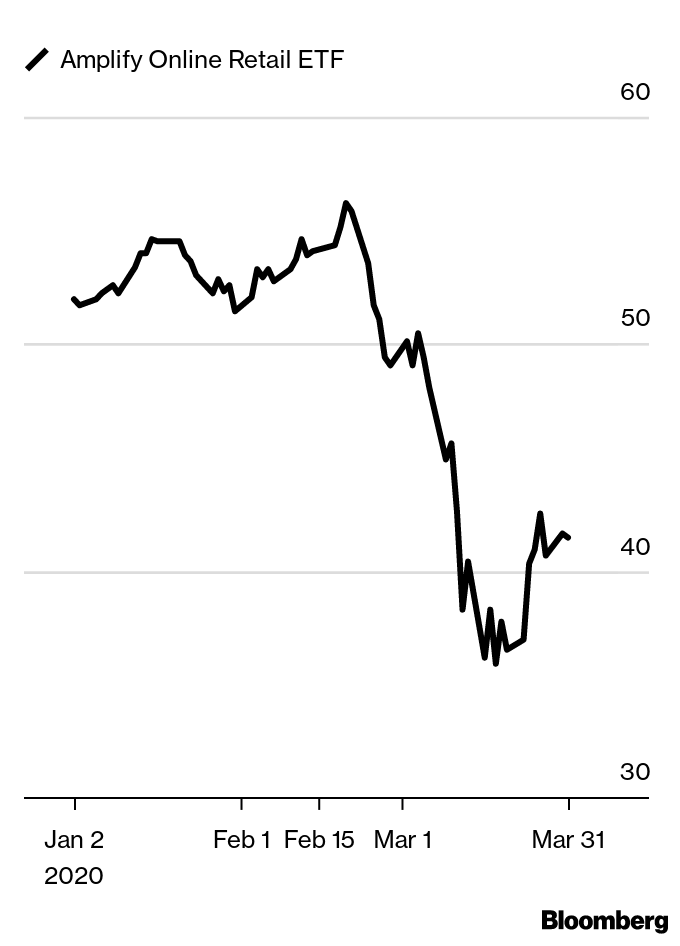

Performance of last quarter’s ETF plays: The Vanguard Consumer Discretionary ETF (VCR) and Amplify Online Retail ETF (IBUY)

and Amplify Online Retail ETF (IBUY) fell 23.3% and 19.2%, respectively, in the first quarter.

fell 23.3% and 19.2%, respectively, in the first quarter.

Focus on the U.S. Consumer